robbyrobinson's blog

Global Bioenergy Industry: Key Statistics and Insights in 2025-2033

Summary:

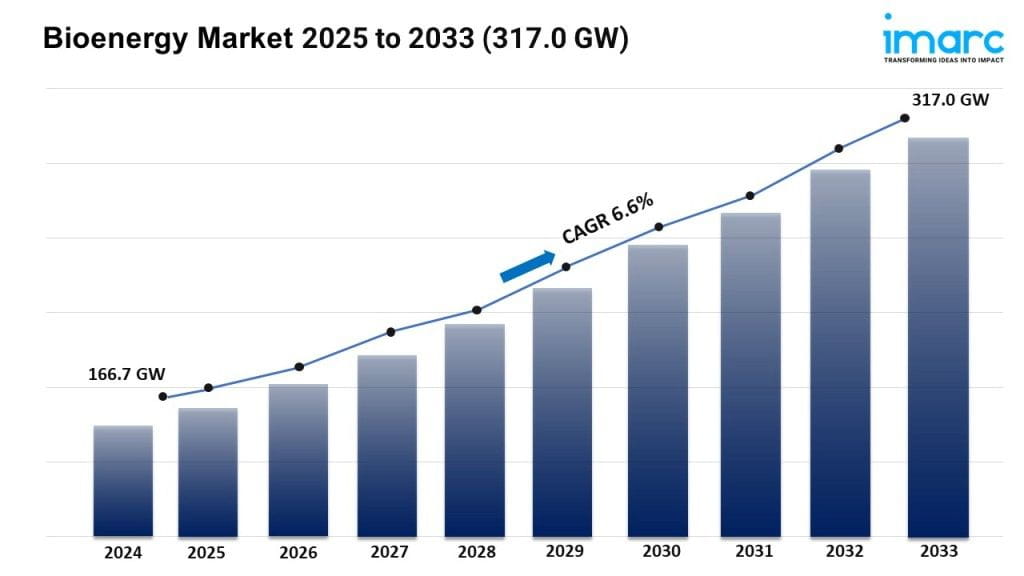

- The global bioenergy market size reached 166.7 GW in 2024.

- The market is expected to reach 317.0 GW by 2033, exhibiting a growth rate (CAGR) of 6.6% during 2025-2033.

- Europe leads the market, accounting for the largest bioenergy market share.

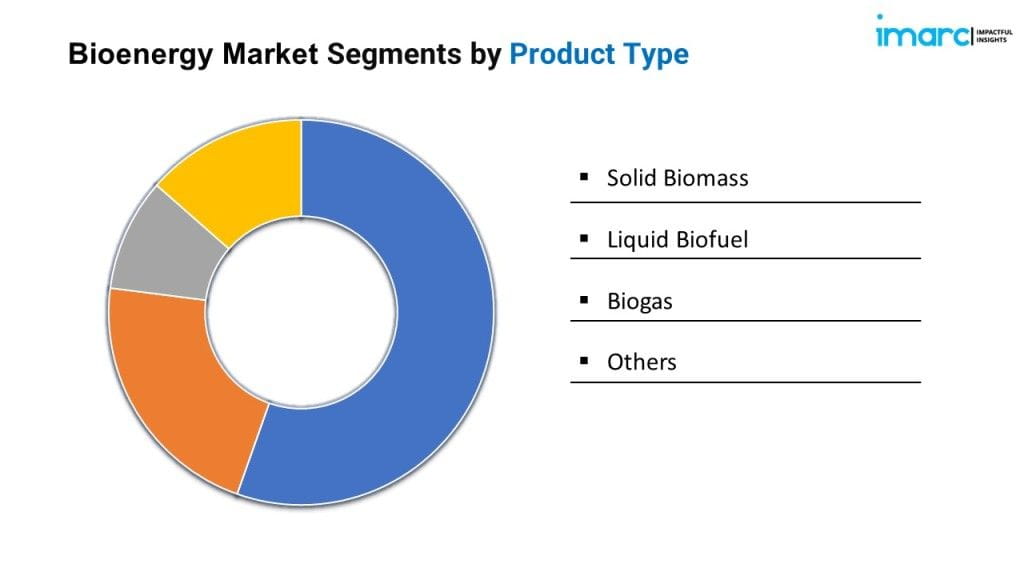

- Due to worries about the detrimental effects of conventional fossil fuels, liquid biofuel holds the largest market share in the product type group.

- The bioenergy industry's primary component is solid waste.

- Because of the growing need for a sustainability in transportation applications, the transportation sector continues to dominate the market.

- One of the main factors propelling the bioenergy industry is a growing environmental concerns.

- The market for bioenergy is changing as a result of rising energy demand and technological developments.

Industry Trends and Drivers:

- Increasing environmental concerns:

The utilization of organic materials, including crop residues, forestry waste, and organic municipal trash, makes bioenergy a renewable energy source. These materials emit fewer greenhouse gases when they are transformed into biofuels or used to generate biopower than fossil fuels like coal, oil, and natural gas. The fight against climate change, a serious environmental issue, is aided by this emission decrease. Moreover, the burning of fossil fuels emits chemicals that lead to respiratory ailments and air pollution, such as sulfur dioxide, nitrogen oxides, and particulate matter. However, because bioenergy technologies emit fewer harmful pollutants, air quality is improved and the negative effects of pollution on the environment and human health are lessened.

- Rising energy demand:

As the demand for energy is rising worldwide, there is a growing concern about ensuring a stable and secure energy supply. Bioenergy contributes to energy security by diversifying the energy mix and reducing dependence on finite fossil fuel resources, which may be subject to geopolitical uncertainties and supply disruptions. In addition, bioenergy can be produced from a wide range of organic materials, including agricultural residues, forestry waste, energy crops, and organic municipal solid waste. These biomass resources are often locally available and renewable, providing a reliable and sustainable source of energy to meet the growing demand, particularly in regions with abundant biomass resources.

- Technological advancements:

Innovations in biomass conversion processes, such as pyrolysis, gasification, and fermentation, are leading to higher yields of bioenergy products like biofuels and biogas. These advancements enhance the overall efficiency of bioenergy production and make it more economically viable. Furthermore, the development of biorefineries, which integrate multiple biomass conversion processes to produce a variety of bio-based products, is expanding the market opportunities for bioenergy. Biorefineries enable the efficient utilization of diverse feedstocks and the maximization of value-added product streams, driving innovations and competitiveness in the bioenergy sector.

Grab a sample PDF of this report: https://www.imarcgroup.com/bioenergy-market/requestsample

Bioenergy Market Report Segmentation:

Breakup By Product Type:

- Solid Biomass

- Liquid Biofuel

- Biogas

- Others

Liquid biofuel represents the largest segment as it offers a direct substitute for conventional fossil fuels like gasoline and diesel, making them more readily adoptable within existing infrastructure and transportation systems.

Breakup By Feedstock:

- Agricultural Waste

- Wood Waste

- Solid Waste

- Others

Solid waste accounts for the majority of the market share due to the abundance of this waste, including organic materials like agricultural residue, forestry waste, and municipal solid waste, which presents a readily available and often underutilized resource for bioenergy production.

Breakup By Region:

- North America (United States, Canada)

- Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, Others)

- Europe (Germany, France, United Kingdom, Italy, Spain, Russia, Others)

- Latin America (Brazil, Mexico, Others)

- Middle East and Africa

Europe enjoys the leading position in the bioenergy market on account of favorable government policies, robust infrastructure, and a strong commitment to renewable energy.

Top Bioenergy Market Leaders:

The bioenergy market research report outlines a detailed analysis of the competitive landscape, offering in-depth profiles of major companies. Some of the key players in the market are:

- Archer-Daniels-Midland Company

- Babcock & Wilcox Enterprises Inc.

- Bunge limited

- EnviTec Biogas AG

- Fortum Oyj

- Hitachi Zosen Corporation

- Mitsubishi Heavy Industries Ltd.

- MVV Energie AG

- Ørsted A/S

- Pacific BioEnergy

- POET LLC

If you require any specific information that is not covered currently within the scope of the report, we will provide the same as a part of the customization.

About Us:

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provide a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: [email protected]

Tel No:(D) +91 120 433 0800

United States: +1-631-791-1145

Global Bioenergy Industry: Key Statistics and Insights in 2025-2033

Summary:

- The global bioenergy market size reached 166.7 GW in 2024.

- The market is expected to reach 317.0 GW by 2033, exhibiting a growth rate (CAGR) of 6.6% during 2025-2033.

- Europe leads the market, accounting for the largest bioenergy market share.

- Due to worries about the detrimental effects of conventional fossil fuels, liquid biofuel holds the largest market share in the product type group.

- The bioenergy industry's primary component is solid waste.

- Because of the growing need for a sustainability in transportation applications, the transportation sector continues to dominate the market.

- One of the main factors propelling the bioenergy industry is a growing environmental concerns.

- The market for bioenergy is changing as a result of rising energy demand and technological developments.

Industry Trends and Drivers:

- Increasing environmental concerns:

The utilization of organic materials, including crop residues, forestry waste, and organic municipal trash, makes bioenergy a renewable energy source. These materials emit fewer greenhouse gases when they are transformed into biofuels or used to generate biopower than fossil fuels like coal, oil, and natural gas. The fight against climate change, a serious environmental issue, is aided by this emission decrease. Moreover, the burning of fossil fuels emits chemicals that lead to respiratory ailments and air pollution, such as sulfur dioxide, nitrogen oxides, and particulate matter. However, because bioenergy technologies emit fewer harmful pollutants, air quality is improved and the negative effects of pollution on the environment and human health are lessened.

- Rising energy demand:

As the demand for energy is rising worldwide, there is a growing concern about ensuring a stable and secure energy supply. Bioenergy contributes to energy security by diversifying the energy mix and reducing dependence on finite fossil fuel resources, which may be subject to geopolitical uncertainties and supply disruptions. In addition, bioenergy can be produced from a wide range of organic materials, including agricultural residues, forestry waste, energy crops, and organic municipal solid waste. These biomass resources are often locally available and renewable, providing a reliable and sustainable source of energy to meet the growing demand, particularly in regions with abundant biomass resources.

- Technological advancements:

Innovations in biomass conversion processes, such as pyrolysis, gasification, and fermentation, are leading to higher yields of bioenergy products like biofuels and biogas. These advancements enhance the overall efficiency of bioenergy production and make it more economically viable. Furthermore, the development of biorefineries, which integrate multiple biomass conversion processes to produce a variety of bio-based products, is expanding the market opportunities for bioenergy. Biorefineries enable the efficient utilization of diverse feedstocks and the maximization of value-added product streams, driving innovations and competitiveness in the bioenergy sector.

Grab a sample PDF of this report: https://www.imarcgroup.com/bioenergy-market/requestsample

Bioenergy Market Report Segmentation:

Breakup By Product Type:

- Solid Biomass

- Liquid Biofuel

- Biogas

- Others

Liquid biofuel represents the largest segment as it offers a direct substitute for conventional fossil fuels like gasoline and diesel, making them more readily adoptable within existing infrastructure and transportation systems.

Breakup By Feedstock:

- Agricultural Waste

- Wood Waste

- Solid Waste

- Others

Solid waste accounts for the majority of the market share due to the abundance of this waste, including organic materials like agricultural residue, forestry waste, and municipal solid waste, which presents a readily available and often underutilized resource for bioenergy production.

Breakup By Region:

- North America (United States, Canada)

- Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, Others)

- Europe (Germany, France, United Kingdom, Italy, Spain, Russia, Others)

- Latin America (Brazil, Mexico, Others)

- Middle East and Africa

Europe enjoys the leading position in the bioenergy market on account of favorable government policies, robust infrastructure, and a strong commitment to renewable energy.

Top Bioenergy Market Leaders:

The bioenergy market research report outlines a detailed analysis of the competitive landscape, offering in-depth profiles of major companies. Some of the key players in the market are:

- Archer-Daniels-Midland Company

- Babcock & Wilcox Enterprises Inc.

- Bunge limited

- EnviTec Biogas AG

- Fortum Oyj

- Hitachi Zosen Corporation

- Mitsubishi Heavy Industries Ltd.

- MVV Energie AG

- Ørsted A/S

- Pacific BioEnergy

- POET LLC

If you require any specific information that is not covered currently within the scope of the report, we will provide the same as a part of the customization.

About Us:

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provide a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: [email protected]

Tel No:(D) +91 120 433 0800

United States: +1-631-791-1145

Global Cancer Biomarkers Industry: Key Statistics and Insights in 2025-2033

Summary:

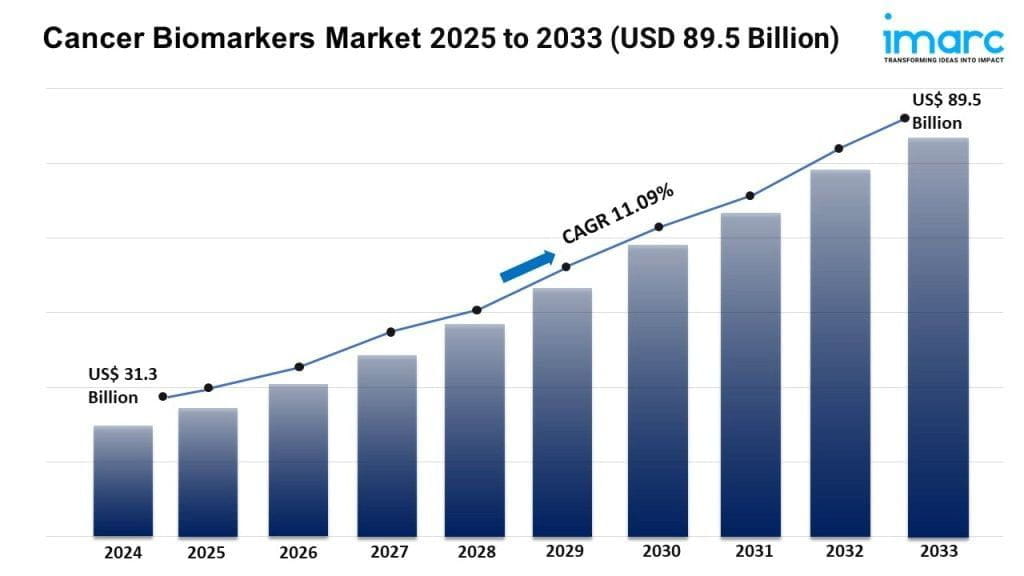

- The global cancer biomarkers market size reached USD 31.3 Billion in 2024.

- The market is expected to reach USD 89.5 Billion by 2033, exhibiting a growth rate (CAGR) of 11.09% during 2025-2033.

- North America leads the market, accounting for the largest cancer biomarkers market share.

- The rise of digital health technologies, like wearable devices and mobile health apps, offers new chances for monitoring biomarkers in real-time, which greatly improves patient engagement and personalized care.

- These innovations allow for ongoing collection of physiological and health-related data, making it possible to find new biomarkers and catch diseases early, when they can be treated.

- Research into unusual sources of biomarkers, such as the microbiome and exosomes, is uncovering new and promising ways to detect and manage cancer.

- Research suggests that the connection between the human microbiome and certain cancers could lead to microbial biomarkers being used as new diagnostic and therapeutic targets.

- The integration of advanced digital health tools and new biomarker sources is changing the way patient care and disease management work.

Industry Trends and Drivers:

- Increasing Prevalence of Cancer:

The increasing prevalence of various cancers is a major factor driving market expansion. As cancer rates rise, we must focus on early detection and diagnosis. We also need to monitor treatment. All of these depend on biomarkers. Cancer biomarkers offer key insights into the disease's biology. They allow for better, tailored treatments that greatly improve patient outcomes. The rise in cancer cases is driving R&D to find new biomarkers. They should predict cancer progression, treatment response, and patient prognosis. This focus on early detection and personalized treatments shows the key role of cancer biomarkers in modern oncology. It also encourages the development of diagnostic tools.

- Advancements in Biomarker Technologies:

Next-gen sequencing (NGS), liquid biopsies, and better imaging are revolutionizing biomarker work. They're transforming identification, analysis, and clinical applications. These advancements improve sensitivity, specificity, and speed in detecting and measuring biomarkers in a variety of biological samples, including blood, tissue, and urine. Early identification of cancer, even before symptoms appear, increases the likelihood of successful therapy and patient survival. AI and ML algorithms enhance biomarker analysis. They boost the accuracy of diagnostic and prognostic models. These technologies improve cancer detection and treatment. Moreover, they open the door to discovering new therapeutic targets.

- Government Initiatives and Funding for Cancer Research:

Several countries' health organizations and governments are investing heavily in cancer research. They aim to enhance care and outcomes. This funding supports projects that explore cancer's molecular causes. It also aids in developing and testing new biomarkers. Public-private partnerships (PPPs) are now more common. They encourage collaboration among government agencies, universities, and biopharmaceutical companies. These agreements speed up the translation of research discoveries into clinical practice, allowing breakthrough diagnostic tests and therapies to reach the market faster. Also, government support for biomarker research attracts private investment. This boosts cancer biomarker innovation.

Grab a sample PDF of this report: https://www.imarcgroup.com/cancer-biomarkers-market/requestsample

Cancer Biomarkers Market Report Segmentation:

By Profiling Technology:

- Omic Technologies

- Imaging Technologies

- Immunoassays

- Cytogenetics

Based on the profiling technology, the market has been divided into omic technologies, imaging technologies, immunoassays, and cytogenetics.

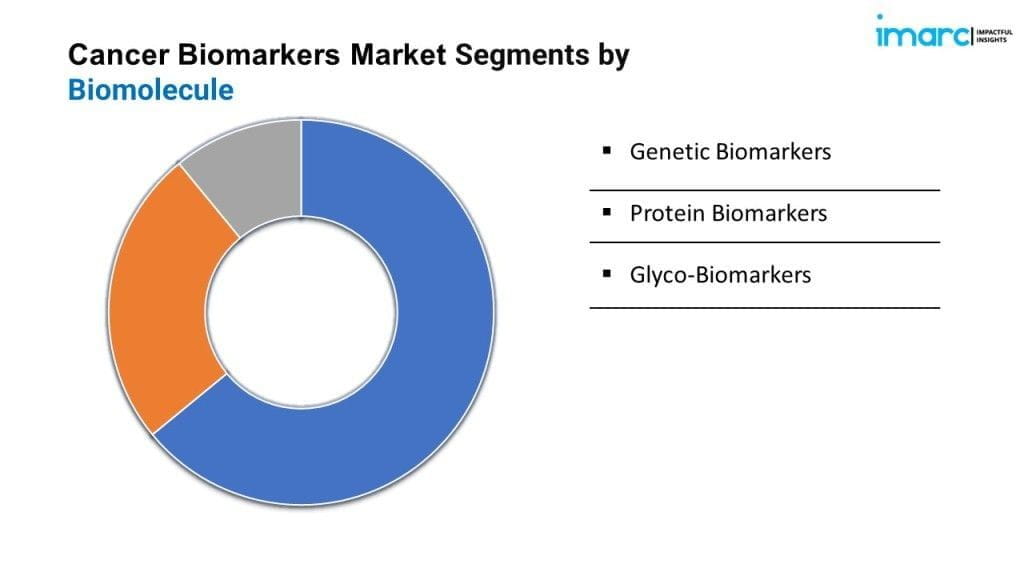

By Biomolecule:

- Genetic Biomarkers

- Protein Biomarkers

- Glyco-Biomarkers

Genetic biomarkers represent the largest segment due to their ability to provide precise information about the genetic makeup of an individual, aiding in personalized treatment approaches.

Breakup By Region:

- North America (United States, Canada)

- Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, Others)

- Europe (Germany, France, United Kingdom, Italy, Spain, Russia, Others)

- Latin America (Brazil, Mexico, Others)

- Middle East and Africa

North America dominates the market attributed to the existence of advanced healthcare infrastructure, rising investment in research and development (R&D), and early adoption of advanced diagnostic technologies in the region.

Top Cancer Biomarkers Market Leaders:

The cancer biomarkers market research report outlines a detailed analysis of the competitive landscape, offering in-depth profiles of major companies. Some of the key players in the market are:

- Abbott Laboratories

- Agilent Technologies Inc.

- Becton Dickinson and Company

- bioMérieux SA

- Danaher Corporation

- F. Hoffmann-La Roche AG

- General Electric Company

- Illumina Inc.

- Qiagen N.V.

- Sino Biological Inc.

- Thermo Fisher Scientific Inc.

If you require any specific information that is not covered currently within the scope of the report, we will provide the same as a part of the customization.

About Us:

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provide a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: [email protected]

Tel No:(D) +91 120 433 0800

United States: +1-631-791-1145

Global E-Paper Display Industry: Key Statistics and Insights in 2025-2033

Summary:

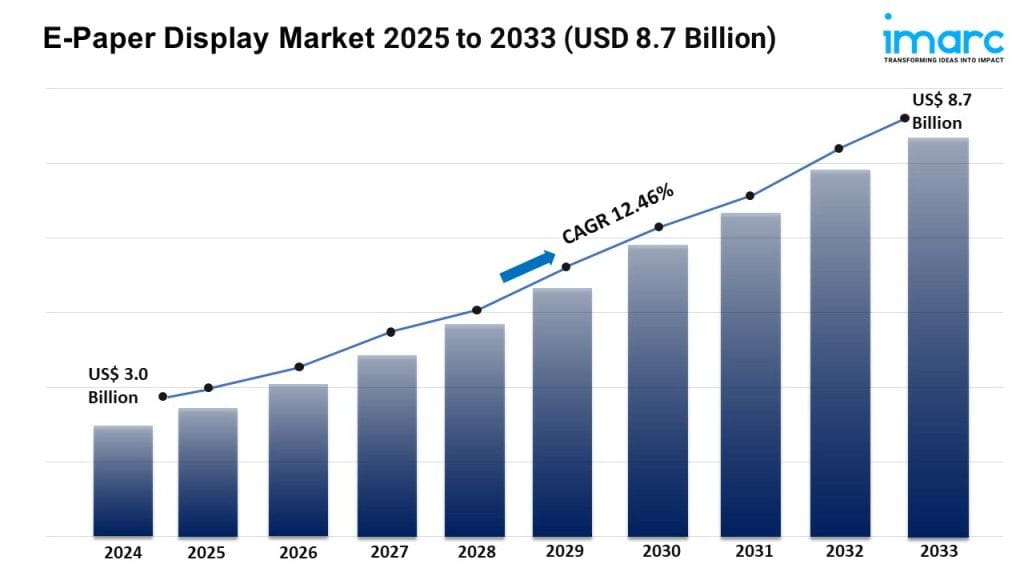

- The global e-paper display market size reached USD 3.0 Billion in 2024.

- The market is expected to reach USD 8.7 Billion by 2033, exhibiting a growth rate (CAGR) of 12.46% during 2025-2033.

- Europe leads the market, accounting for the largest e-paper display market share.

- E-readers make up most of the market share in this product segment because people increasingly want portable and convenient ways to read.

- The largest share of the e-paper display industry belongs to consumer electronics.

- The main factor driving the e-paper display market is the growing demand for low-power displays.

- Advances in technology and growth in the retail and advertising sectors are changing the market for e-paper displays.

Industry Trends and Drivers:

- Expansion In Retail and Advertising Sectors:

E-paper displays are gaining popularity in retail and advertising, thanks to their unique characteristics and benefits that match the evolving needs of these sectors. E-paper displays offer high visibility in various lighting conditions, including direct sunlight. This feature is especially useful in retail and advertising, where clear and easy-to-read displays are essential. Unlike traditional digital screens, e-paper works like regular paper, reflecting light to provide a more readable and less harsh experience. This makes them ideal for window displays and outdoor advertising, where visibility is a key concern. E-paper displays have a significant advantage in the retail and advertising sectors because they support dynamic content updates. Retailers can easily update prices, promotions, or product information without physical reprints. Similarly, advertisers can change the content in real time to reflect current campaigns or offers. This flexibility makes it possible to deliver targeted and timely messages, which boosts user engagement and response rates.

- Technological Advancements:

Recent advancements in e-paper technology are leading to significant improvements in performance, flexibility, and application. Innovations in color e-paper technology are enhancing the visual appeal and versatility of e-paper displays. Traditional e-paper screens, primarily in black and white, are now being supplemented with color capabilities. Key players are developing color e-paper displays that use advanced microencapsulation techniques to achieve a wider color gamut and higher resolution. These color displays are increasingly used in e-readers, digital signage, and electronic shelf labels, offering users a more vibrant and engaging visual experience. In addition, high-resolution e-paper displays offer sharper text and images that improve readability and user experience. Advancements in electronic ink technology and display manufacturing processes are improving contrast ratios. This progress allows e-paper screens to deliver clearer and more detailed content.

- Rising Demand for Low-Power Displays:

E-paper displays are inherently energy-efficient, consuming minimal power as compared to traditional liquid-crystal display (LCD) or organic light-emitting diodes (OLED) screens. This characteristic aligns with the rising demand for low-power and eco-friendly technologies in consumer electronics. E-paper displays only consume power when the image on the screen changes. Once the image is set, no additional power is needed to maintain it. In contrast, LCDs and OLEDs require a constant power supply to keep the image visible. E-paper utilizes bi-stable display technology. This means that once an image is displayed, it remains on the screen without needing ongoing power to maintain it. This is different from traditional displays that require constant power to keep the screen active.

Grab a sample PDF of this report: https://www.imarcgroup.com/e-paper-display-market/requestsample

E-Paper Display Market Report Segmentation:

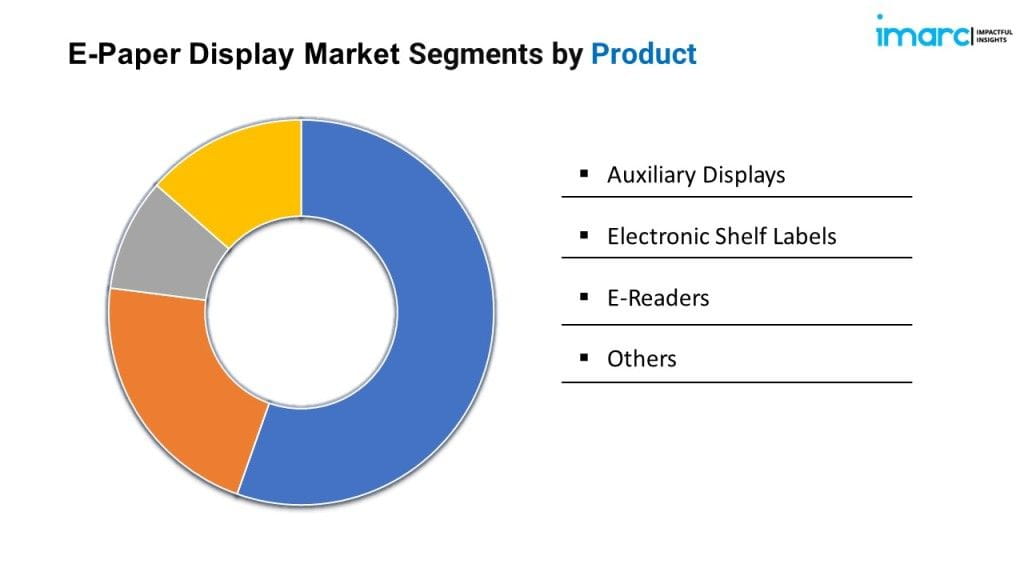

Breakup By Product:

- Auxiliary Displays

- Electronic Shelf Labels

- E-Readers

- Others

E-readers account for the majority of shares on account of the rising demand for portable and convenient reading solutions.

Breakup By Application:

- Consumer Electronics

- Healthcare

- Institutional

- Media and Entertainment

- Transportation

- Others

Consumer electronics dominate the market due to the increasing adoption of energy-efficient devices, including smartwatches and fitness trackers.

Breakup By Region:

- North America (United States, Canada)

- Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, Others)

- Europe (Germany, France, United Kingdom, Italy, Spain, Russia, Others)

- Latin America (Brazil, Mexico, Others)

- Middle East and Africa

Europe enjoys the leading position owing to a large market for e-paper display driven by the rising focus on sustainability and energy conservation.

Top E-Paper Display Market Leaders:

The e-paper display market research report outlines a detailed analysis of the competitive landscape, offering in-depth profiles of major companies. Some of the key players in the market are:

- Adafruit Industries LLC

- CLEARink Displays Inc.

- E Ink Holdings Inc.

- Hanvon Technology Co. Ltd.

- LANCOM Systems GmbH (Rohde & Schwarz GmbH & Co KG)

- Microtips Technology

- Pervasive Displays Inc. (SES-imagotag)

- Plastic Logic (FlexEnable Limited)

- Toppan Inc.

- Visionect

If you require any specific information that is not covered currently within the scope of the report, we will provide the same as a part of the customization.

About Us:

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provide a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: [email protected]

Tel No:(D) +91 120 433 0800

United States: +1-631-791-1145

Global Urology Robotic Surgery Industry: Key Statistics and Insights in 2025-2033

Summary:

- The global urology robotic surgery market size reached USD 2.0 Billion in 2024.

- The market is expected to reach USD 4.3 Billion by 2033, exhibiting a growth rate (CAGR) of 8.71% during 2025-2033.

- North America's leads the market, accounting for the largest urology robotic surgery market share.

- Ongoing advancements in robotic technology are driving market growth.

- These innovations enhance the precision, flexibility, and range of motion of surgical instruments, surpassing the limitations of human hands.

- The increasing prevalence of urological disorders worldwide, such as prostate cancer, bladder cancer, and kidney stones, is driving the demand for robotic urology surgeries.

- Instruments and accessories dominate the market due to their ability to enhance precision and control.

- Robotic prostatectomy dominates the market due to its precise surgical capabilities.

Grab a sample PDF of this report: https://www.imarcgroup.com/urology-robotic-surgery-market/requestsample

Industry Trends and Drivers:

- Advancements in Robotic Technology:

The continuous advancement in robotic technology is impelling the growth of the market. These innovations enhance the precision, flexibility, and range of motion of surgical instruments, transcending the limitations of human hands. Robotic systems are setting high standards for accuracy, reducing the likelihood of post-surgical complications and improving patient outcomes. The integration of high-definition 3D vision systems and software updates further refines the abilities of surgeons to perform complex urological procedures with enhanced dexterity and control. As technology evolves, the incorporation of artificial intelligence (AI) and machine learning (ML) is offering predictive analytics, improving surgical efficiency and patient-specific customization.

- Increasing Prevalence of Urological Disorders:

The global rise in urological disorders, including prostate cancer, bladder cancer, and kidney stones, is driving the demand for robotic urology surgeries. These conditions require precise and minimally invasive (MI) interventions, which robotic surgery can provide. The high success rate, reduced pain, quicker recovery, and lower risk of infection associated with robotic-assisted surgeries make them a preferred choice for both surgeons and patients. As the aging population is growing, the occurrence of urological conditions is increasing. Early detection and evolving healthcare infrastructure also contribute to the expanding adoption of robotic surgical systems, encouraging advancements in surgical techniques.

- Economic and Regulatory Support:

Financial investment in healthcare infrastructure, along with favorable reimbursement policies, plays a crucial role in the adoption of urology robotic surgery systems. Governments and healthcare organizations are recognizing the long-term benefits of robotic-assisted surgeries, such as reduced hospital stays, lower readmission rates, and decreased post-operative complications, which in turn are leading to significant healthcare cost savings. Moreover, regulatory approvals for advanced robotic systems are increasing their market introduction and adoption. The support in terms of funding for research and development (R&D) from both public and private sectors encourages continuous innovation, ensuring the availability of advanced, more efficient, and safer robotic surgical systems.

Explore full report with table of contents: https://www.imarcgroup.com/urology-robotic-surgery-market

Urology Robotic Surgery Market Report Segmentation:

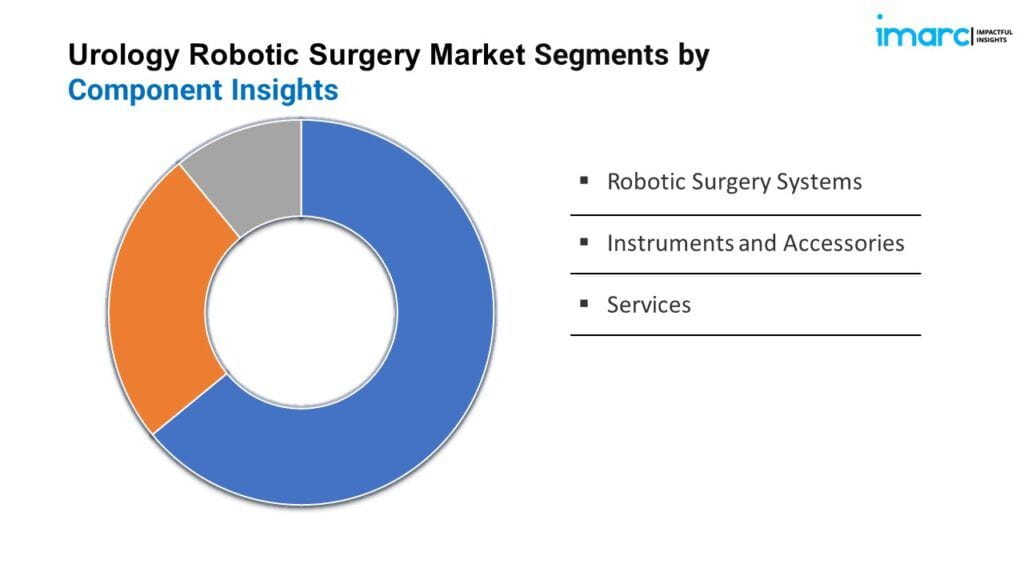

By Component:

- Robotic Surgery Systems

- Instruments and Accessories

- Services

Instruments and accessories represent the largest segment as they offer enhanced precision and control.

By Application:

- Robotic Prostatectomy

- Robotic Cystectomy

- Robotic Pyeloplasty

- Robotic Nephrectomy

- Others

Robotic prostatectomy exhibits a clear dominance in the market due to its efficient surgical precision.

Regional Insights:

- North America (United States, Canada)

- Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, Others)

- Europe (Germany, France, United Kingdom, Italy, Spain, Russia, Others)

- Latin America (Brazil, Mexico, Others)

- Middle East and Africa

North America's dominance in the urology robotic surgery market is attributed to the rising demand for minimally invasive (MI) surgical procedures.

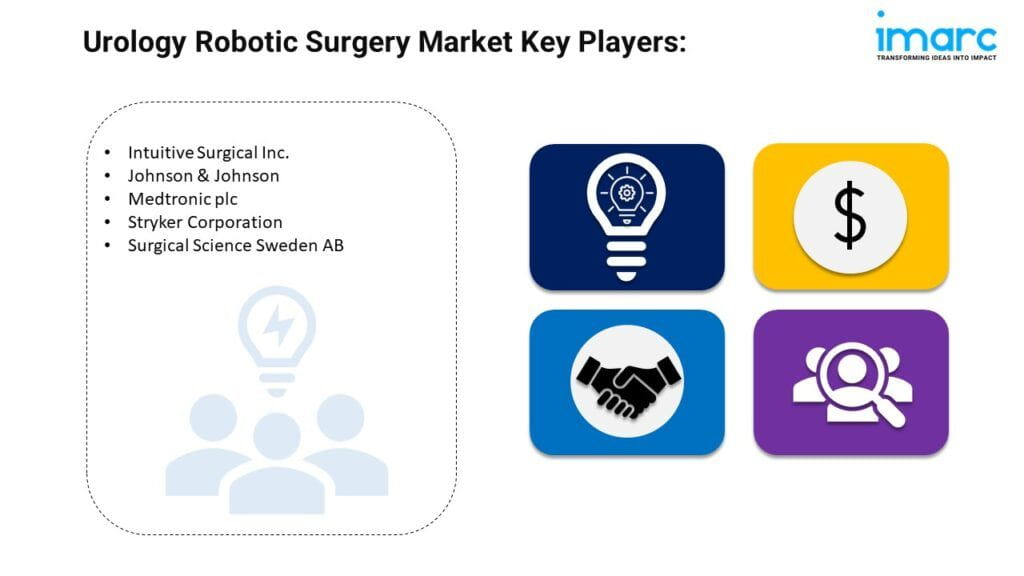

Top Urology Robotic Surgery Market Leaders:

The urology robotic surgery market research report outlines a detailed analysis of the competitive landscape, offering in-depth profiles of major companies. Some of the key players in the market are:

- Intuitive Surgical Inc.

- Johnson & Johnson

- Medtronic plc

- Stryker Corporation

- Surgical Science Sweden AB

If you require any specific information that is not covered currently within the scope of the report, we will provide the same as a part of the customization.

About Us:

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provide a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: [email protected]

Tel No:(D) +91 120 433 0800

United States: +1-631-791-1145

Global Zircon Sand Industry: Key Statistics and Insights in 2025-2033

Summary:

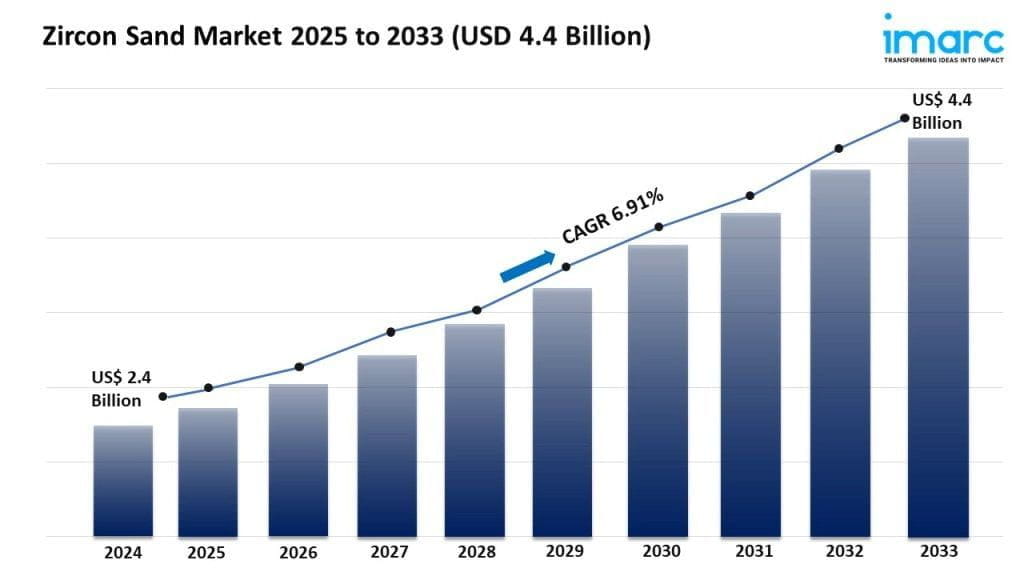

- The global zircon sand market size reached USD 2.4 Billion in 2024.

- The market is expected to reach USD 4.4 Billion by 2033, exhibiting a growth rate (CAGR) of 6.91% during 2025-2033.

- Asia Pacific leads the market, accounting for the largest zircon sand market share.

- Colorless leads the market share in this product segment because it has versatile properties, making it suitable for use in a variety of products, such as tiles, sanitary ware, and high-end glass products.

- The building and construction industry holds the largest market share in zircon sand.

- The thriving ceramic industry is a major driver of the zircon sand market.

- The use of zircon sand in refractory applications is on the rise, and this shift is impacting the zircon sand market.

Grab a sample PDF of this report: https://www.imarcgroup.com/zircon-sand-market/requestsample

Industry Trends and Drivers:

- Ceramic industry growth:

As the construction industry is expanding, there is rise in the demand for ceramic products like tiles, sanitary ware, and tableware. Zircon sand is essential in the production of these ceramics due to its high melting point, strength, and durability, which enhance the performance and longevity of ceramic items. Zircon sand is used to produce high-performance ceramics with superior properties, such as thermal stability, resistance to abrasion, and chemical inertness. This makes it valuable for specialized applications, including industrial ceramics used in harsh environments, which are demanded in various industrial sectors. Technological advancements in ceramic manufacturing processes, including the development of new ceramic materials and improved production techniques, often involve the use of zircon sand. These advancements are driving innovations and increasing the consumption of zircon sand.

- Refractory applications:

Zircon sand has a high melting point and excellent thermal stability, making it ideal for use in refractory materials that must withstand extreme temperatures. This property is crucial in industries such as steelmaking, glass production, and petrochemical processing, where refractory materials are exposed to high heat. The steel and glass industries are major consumers of refractory materials. As global demand for steel and glass is increasing, so does the demand for zircon sand, which is used in producing refractory linings, casting molds, and other high-temperature applications. Innovations in refractory materials, including the development of advanced and specialized refractories, often incorporate zircon sand. These advancements aim to improve the performance, longevity, and efficiency of refractory products, driving the demand for zircon sand.

- Technological advancements:

Innovations in mining and processing technologies are improving the efficiency and yield of zircon sand extraction. New methods can reduce costs, increase production, and enhance the quality of zircon sand, making it more attractive to manufacturers and end-users. Innovations in zircon sand processing have led to the creation of high-performance zircon-based materials. These materials are used in various advanced applications, including high-temperature and corrosive environments, which increases demand for zircon sand. Technological advancements in refractory materials, such as the development of more durable and efficient refractories, often incorporate zircon sand. Enhanced refractory materials offer better thermal resistance and longevity, driving the need for high-quality zircon sand.

Explore full report with table of contents: https://www.imarcgroup.com/zircon-sand-market

Zircon Sand Market Report Segmentation:

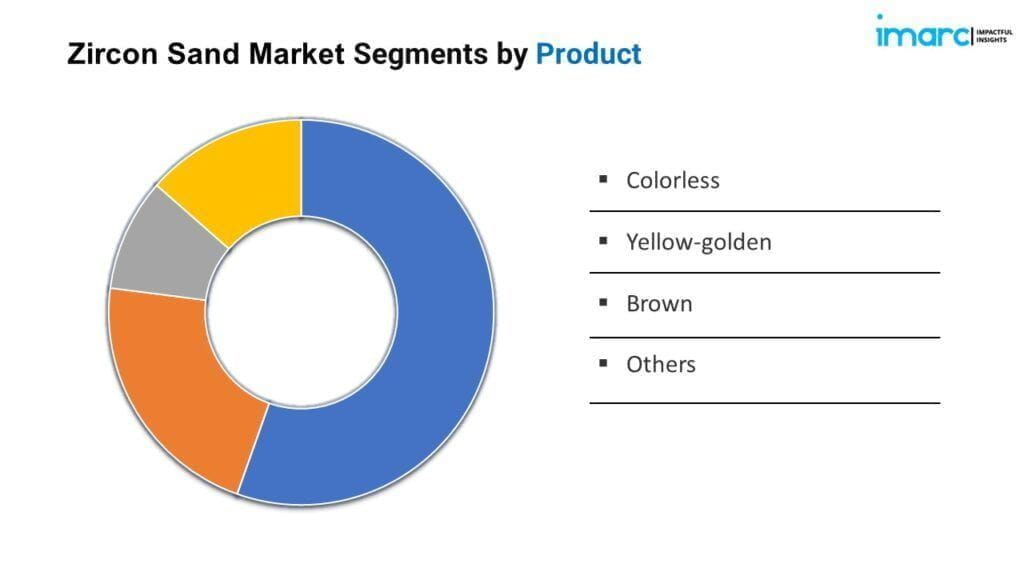

Breakup By Product:

- Colorless

- Yellow-golden

- Brown

- Others

Colorless represents the largest segment due to its high purity and versatility in applications such as ceramics and refractories, which drives its dominant market share.

Breakup By Industry Vertical:

- Foundry Industry

- Refractory Industry

- Ceramic Industry

- Medical and Healthcare Industry

- Building and Construction Industry

Building and construction industry account for the majority of the market share because it is essential in producing high-quality ceramic tiles and sanitary ware, which are critical for construction and renovation projects.

Breakup By Region:

- North America (United States, Canada)

- Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, Others)

- Europe (Germany, France, United Kingdom, Italy, Spain, Russia, Others)

- Latin America (Brazil, Mexico, Others)

- Middle East and Africa

Asia Pacific enjoys the leading position in the zircon sand market owing to its strong manufacturing base, significant demand from the rapidly growing construction and ceramics sectors, and major zircon sand-producing countries like Australia and China.

Top Zircon Sand Market Leaders:

The zircon sand market research report outlines a detailed analysis of the competitive landscape, offering in-depth profiles of major companies. Some of the key players in the market are:

- Eramet

- Foskor Zirconia (PTY) Limited

- Iluka Resources Limited

- Kenmare Resources plc

- Luxfer MEL Technologies (Luxfer Group)

- Rio Tinto

- Tronox Holdings plc

If you require any specific information that is not covered currently within the scope of the report, we will provide the same as a part of the customization.

About Us:

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provide a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: [email protected]

Tel No:(D) +91 120 433 0800

United States: +1-631-791-1145

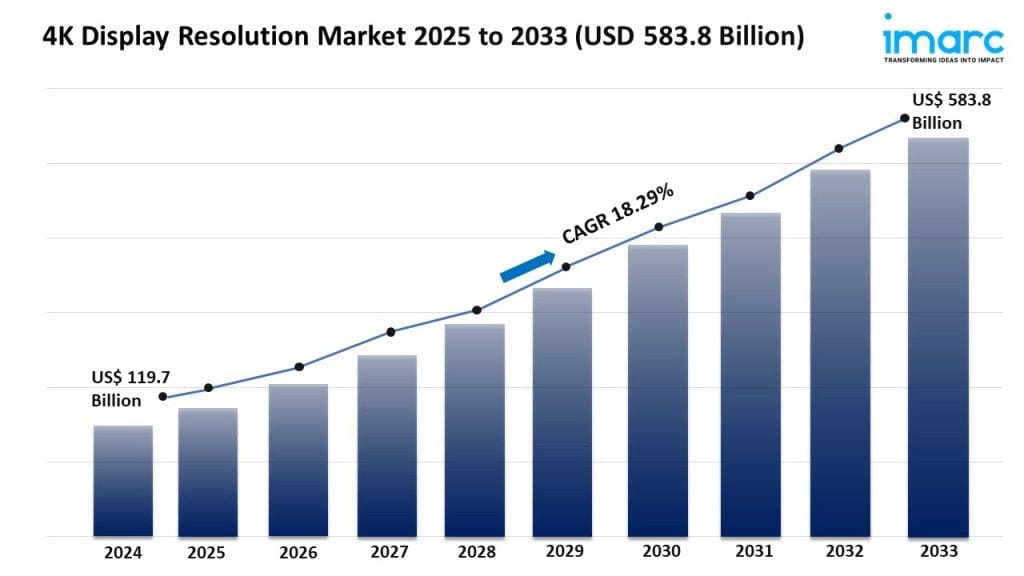

Global 4K Display Resolution Industry: Key Statistics and Insights in 2025-2033

Summary:

- The global 4K display resolution market size reached USD 119.7 Billion in 2024.

- The market is expected to reach USD 583.8 Billion by 2033, exhibiting a growth rate (CAGR) of 18.29% during 2025-2033.

- Asia Pacific leads the market, accounting for the largest 4K display resolution market share.

- Smart TVs dominate the market because they offer easy access to a vast range of content without needing extra devices.

- The entertainment and media industry is the market leader, fueled by the growing popularity of streaming services, social media, and online gaming.

- The popularity of streaming services, gaming, and content creation is driving up demand for high-resolution content, which is in turn fueling market growth.

- Thanks to technological advancements, manufacturers can now produce 4K displays that are more efficient, perform better, and cost less.

- The global rise in popularity of devices capable of 4K is driving market growth.

Industry Trends and Drivers:

- Rising Demand for High-Resolution Content:

The rising need for high-resolution content is contributing to the growth of the market. Individuals are increasingly engaging with high-definition content across various platforms, such as streaming services, gaming, and content creation. The increasing demand for displays capable of delivering superior image quality and clarity is propelling the market growth. 4K resolution has higher pixel density as compared to standard HD displays. They provide sharper details, superior-quality colors, and enhanced visual experiences. Furthermore, individuals are willing to invest in 4K displays for enhanced experience.

- Advancements in Digital Technologies:

Innovations in digital technologies enable manufacturers to produce 4K displays with higher efficiency, improved performance, and reduced costs. Advancements in display panel technology, such as organic light-emitting diode (OLED) and quantum dot light emitting diode (QLED), enhance the capabilities of 4K displays by offering deeper blacks, wider color gamuts, and higher contrast ratios, thereby enhancing the overall viewing experience. Additionally, advancements in image processing algorithms and display interfaces optimize the rendering of 4K content, ensuring seamless compatibility and enhanced picture quality. These technological advancements make 4K displays more accessible and affordable to individuals.

- Increasing Adoption of 4K-Capable Devices:

The rising adoption of 4K-capable devices among the masses around the world is bolstering the market growth. People are adopting devices, such as smartphones, tablets, computers, and televisions that support 4K resolution. The increasing focus on enhanced visual experiences and improved productivity, along with the availability of high-resolution content, is supporting the growth of the market. People are seeking displays that can fully leverage the capabilities of their 4K-capable devices. In addition, manufacturers are incorporating 4K resolution into a wider range of products, which is impelling the market growth.

Grab a sample PDF of this report: https://www.imarcgroup.com/4k-display-resolution-market/requestsample

4K Display Resolution Market Report Segmentation:

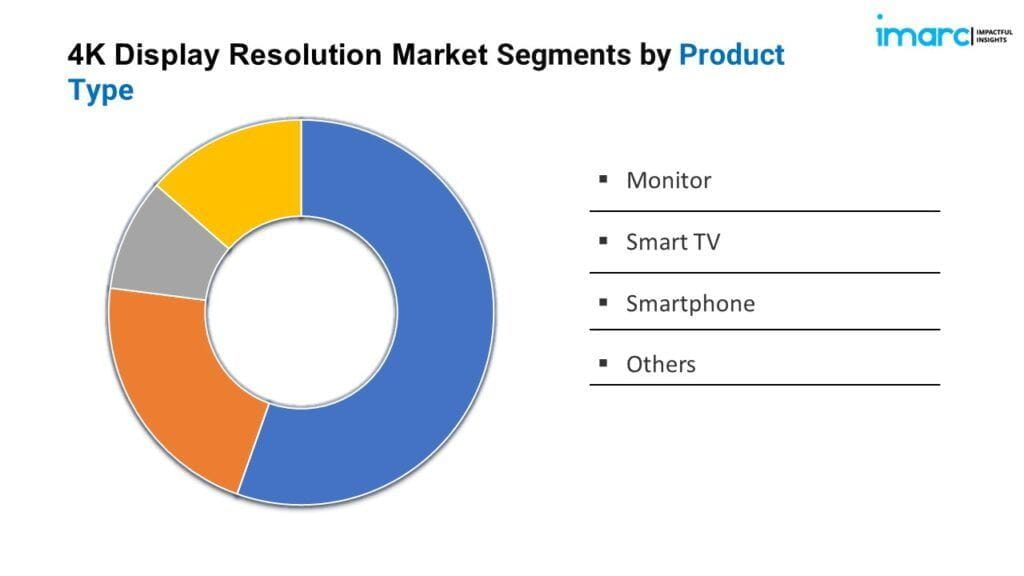

By Product Type:

- Monitor

- Smart TV

- Smartphone

- Others

Smart TV represents the largest segment as it provides easy access to a wide range of content without additional peripherals.

By End User:

- Aerospace and Defence

- Business and Education

- Entertainment and Media

- Retail and Advertisement

- Others

Entertainment and media hold the biggest market share due to the rising utilization of streaming services, social media platforms, and online gaming.

Regional Insights:

- North America (United States, Canada)

- Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, Others)

- Europe (Germany, France, United Kingdom, Italy, Spain, Russia, Others)

- Latin America (Brazil, Mexico, Others)

- Middle East and Africa

Asia Pacific enjoys a leading position in the 4K display resolution market on account of the increasing demand for high-quality entertainment experiences among individuals.

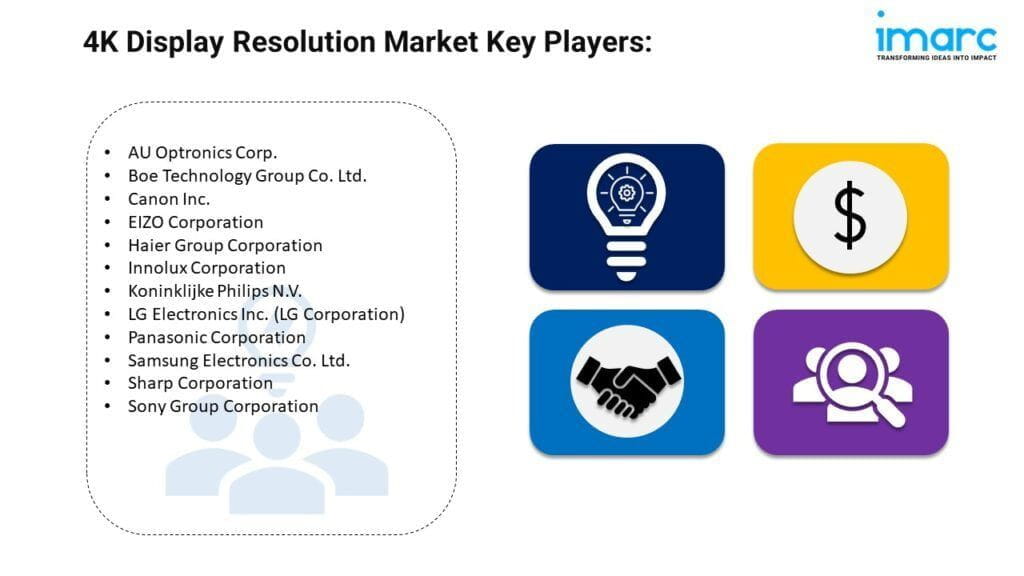

Top 4K Display Resolution Market Leaders:

The 4K display resolution market research report outlines a detailed analysis of the competitive landscape, offering in-depth profiles of major companies. Some of the key players in the market are:

- AU Optronics Corp.

- Boe Technology Group Co. Ltd.

- Canon Inc.

- EIZO Corporation

- Haier Group Corporation

- Innolux Corporation

- Koninklijke Philips N.V.

- LG Electronics Inc. (LG Corporation)

- Panasonic Corporation

- Samsung Electronics Co. Ltd.

- Sharp Corporation

- Sony Group Corporation

If you require any specific information that is not covered currently within the scope of the report, we will provide the same as a part of the customization.

About Us:

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provide a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: [email protected]

Tel No:(D) +91 120 433 0800

United States: +1-631-791-1145

Global Polydextrose Industry: Key Statistics and Insights in 2025-2033

Summary:

- The global polydextrose market size reached USD 315.8 Million in 2024.

- The market is expected to reach USD 469.3 Million by 2033, exhibiting a growth rate (CAGR) of 4.27% during 2025-2033.

- North America leads the market, accounting for the largest polydextrose market share.

- The largest market category consists of baking and confectionery goods, driven by high demand due to changing customer preferences.

- The market is dominated by powdered food additives due to their ease of use and adaptability.

- Polydextrose is a valuable ingredient due to its versatility, making it suitable for use in many different culinary products.

- Growing concern over diabetes and obesity is driving the need for healthier food options with lower calorie and sugar content.

Industry Trends and Drivers:

- Food Industry Applications:

Polydextrose is a beneficial component in many food applications because of its increased versatility. It is extensively utilized in dairy products, confections, beverages, pastry goods, and dietary supplements. In baked goods, it adds fiber content and enhances texture and moisture retention. As a bulking agent, it lets confections use less sugar. This lowers sugar levels without losing flavor or texture. In addition, polydextrose improves mouthfeel and stability in dairy products and beverages. Its use in dietary supplements meets the rising demand for health-boosting functional foods.

- Growing Demand for Low-Calorie and Low-Sugar Products:

Low-calorie and low-sugar food choices are becoming more and more popular as obesity and diabetes become more common. Because polydextrose is a low-calorie and sugar alternative, food makers can create lower-calorie goods without sacrificing flavor or texture. Customers are increasingly choosing goods with polydextrose as they look for healthier eating options without compromising flavor. Because lifestyle diseases are more common in poorer nations, this trend is more important. Furthermore, because polydextrose can replicate the weight and texture of sugar, it is a perfect ingredient for a variety of items, such as snacks, beverages, and baked goods.

- Rising Health Consciousness:

The global population's growing emphasis on health and wellness is driving market expansion. The demand for polydextrose is rising as a result of consumers' growing awareness of the advantages of dietary fiber. The prebiotic qualities of this soluble fiber are well known for supporting gut health by encouraging the growth of good bacteria. The inclusion of polydextrose in everyday diets is a result of the relevance of dietary fiber in reducing chronic diseases like obesity, diabetes, and heart disease. Food producers are encouraged to develop and incorporate functional ingredients like polydextrose into their goods by the trend toward healthier eating habits.

Grab a sample PDF of this report: https://www.imarcgroup.com/polydextrose-market/requestsample

Polydextrose Market Report Segmentation:

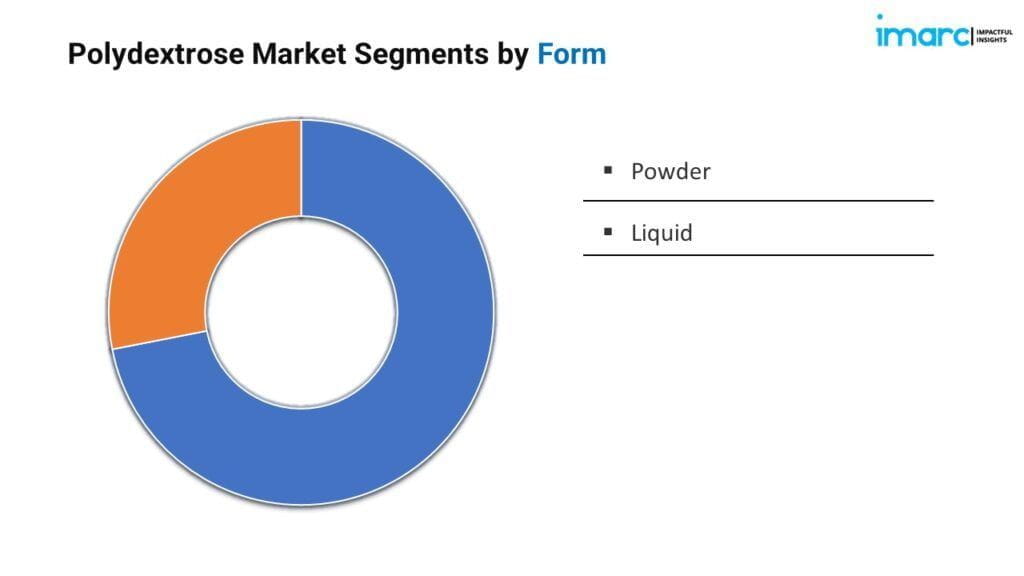

By Form:

- Powder

- Liquid

Powder represents the largest segment as it can be easily incorporated into a wide range of food products.

By Application:

- Bakery and Confectionery

- Beverages

- Yogurts and Dairy Products

- Others

Bakery and confectionery hold the biggest market share due to the changing eating patterns of individuals.

Regional Insights:

- North America (United States, Canada)

- Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, Others)

- Europe (Germany, France, United Kingdom, Italy, Spain, Russia, Others)

- Latin America (Brazil, Mexico, Others)

- Middle East and Africa

Region-wise, the polydextrose market is segmented into North America (the United States and Canada); Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, and others); Europe (Germany, France, the United Kingdom, Italy, Spain, Russia, and others); Latin America (Brazil, Mexico, and others); and the Middle East and Africa.

Top Polydextrose Market Leaders:

The polydextrose market research report outlines a detailed analysis of the competitive landscape, offering in-depth profiles of major companies. Some of the key players in the market are:

- Akhil Healthcare Pvt Ltd

- Baolingbao Biology Co. Ltd.

- Cargill Incorporated

- Danisco A/S (International Flavors & Fragrances Inc.DuPont de Nemours Inc.)

- Devson Impex Private Limited

- Foodchem International Corporation

- Henan Tailijie Biotech Co. Ltd

- Rajvi Enterprise Private Limited

- Samyang Corporation

- Shandong Bailong Chuangyuan Bio-Tech Co. Ltd.

- Tate & Lyle PLC

- Van Wankum Ingredients

If you require any specific information that is not covered currently within the scope of the report, we will provide the same as a part of the customization.

About Us:

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provide a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: [email protected]

Tel No:(D) +91 120 433 0800

United States: +1-631-791-1145

Global Water Dispenser Industry: Key Statistics and Insights in 2025-2033

Summary:

- The global water dispenser market size reached USD 3.0 Billion in 2024.

- The market is expected to reach USD 4.8 Billion by 2033, exhibiting a growth rate (CAGR) of 5.04% during 2025-2033.

- North America leads the market, accounting for the largest water dispenser market share.

- Retail stores make up the largest market for water dispensers, providing consumers with the convenience of buying immediately and having their purchase delivered to their home.

- The commercial sector is the top market for water dispensers, mainly because offices, schools, hospitals, and other public areas need machines that are reliable and can handle a high volume.

- Consumers are growing more aware of the tap water contaminants, such as lead and chlorine, that may be present.

- Innovations such as multi-stage filtration, reverse osmosis, UV purification, and activated carbon filters are making water purer by removing contaminants, microorganisms, and impurities more effectively.

Grab a sample PDF of this report: https://www.imarcgroup.com/water-dispenser-market/requestsample

Industry Trends and Drivers:

- Health and Wellness Awareness:

People are more informed about the potential contaminants in tap water, such as lead, chlorine, and other impurities. This awareness drives the demand for water dispensers that offer filtration and purification features to ensure safe drinking water. The rise in awareness about diseases caused by contaminated water, like cholera, dysentery, and gastrointestinal infections, makes consumers prioritize clean water. Water dispensers with advanced purification technologies provide a reliable solution.

- Technological Advancements:

Innovations, such as multi-stage filtration, reverse osmosis (RO), ultraviolet (UV) purification, and activated carbon filters, ensure higher levels of water purity, removing contaminants, microorganisms, and impurities more effectively. Some modern water dispensers add essential minerals back into the purified water, enhancing its taste and health benefits. Smart water dispensers can connect to the Internet of Things (IoT), allowing users to monitor water quality, filter status, and dispenser performance through mobile apps.

- Urbanization and Lifestyle Changes:

Urban areas have higher population densities, which leads to greater demand for accessible and convenient sources of clean drinking water. Rapid urbanization often brings about improved infrastructure, including water supply systems. However, concerns about tap water quality still drive consumers to seek additional purification options like water dispensers. Urban dwellers often have hectic schedules, making the convenience of instant hot and cold water from dispensers highly appealing.

The water dispenser market report provides a comprehensive overview of the industry. This analysis is essential for stakeholders aiming to navigate the complexities of the biochar market and capitalize on emerging opportunities.

Water Dispenser Market Report Segmentation:

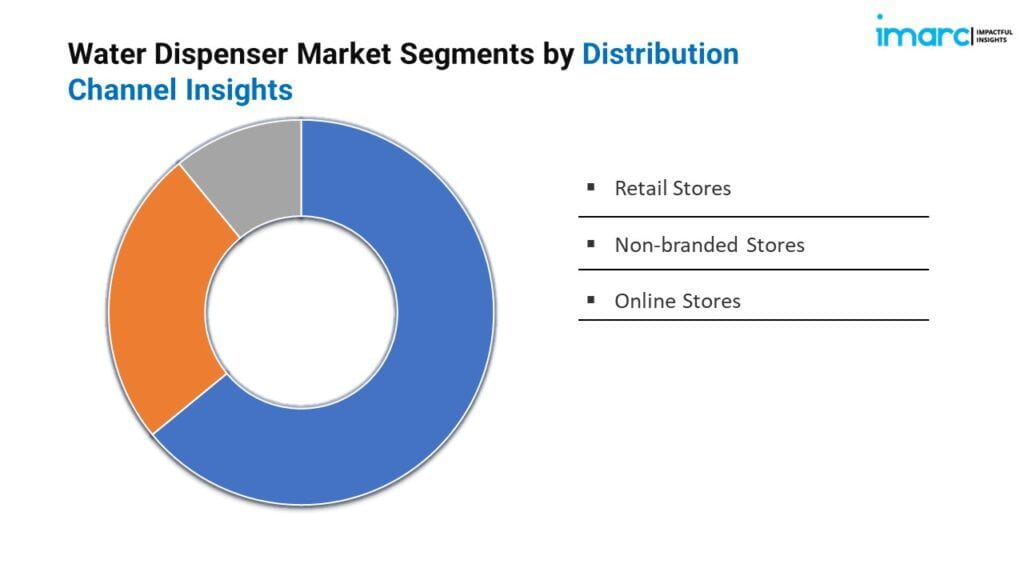

By Distribution Channel:

- Retail Stores

- Non-branded Stores

- Online Stores

Retail stores account for the majority of the market share as they provide immediate access to a variety of water dispenser models, enabling consumers to purchase and take home products directly.

By Application:

- Commercial

- Residential

- Industrial

Commercial exhibits a clear dominance in the market due to the high demand for reliable and large-capacity water dispensers in offices, educational institutions, healthcare facilities, and other public spaces.

Regional Insights:

- North America (United States, Canada)

- Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, Others)

- Europe (Germany, France, United Kingdom, Italy, Spain, Russia, Others)

- Latin America (Brazil, Mexico, Others)

- Middle East and Africa

North America enjoys the leading position in the water dispenser market on account of high consumer awareness, advanced infrastructure, and significant adoption of health and wellness trends.

Top Water Dispenser Market Leaders:

The water dispenser market research report outlines a detailed analysis of the competitive landscape, offering in-depth profiles of major companies. Some of the key players in the market are:

- A. O. Smith Corporation

- Blue Star Limited

- Clover Co. Ltd.

- Culligan Water

- Electrolux AB

- Haier Group Corporation

- Honeywell International Inc.

- Midea Group

- Panasonic Holdings Corporation

- Primo Water Corporation

- The Clorox Company

- Voltas Limited

- Waterlogic Plc

If you require any specific information that is not covered currently within the scope of the report, we will provide the same as a part of the customization.

About Us:

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provide a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: [email protected]

Tel No:(D) +91 120 433 0800

United States: +1-631-791-1145

Global Ovarian Cancer Industry: Key Statistics and Insights in 2025-2033

Summary:

- The global ovarian cancer market size reached USD 2.3 Billion in 2024.

- The market is expected to reach USD 5.5 Billion by 2033, exhibiting a growth rate (CAGR) of 9.59% during 2025-2033.

- North America leads the market, accounting for the largest ovarian cancer market share.

- Most cases of ovarian cancer are epithelial, and they typically affect older women.

- The market has been segmented by end user into hospitals, homecare, specialty centers, and others.

- Advances in diagnostic technology are changing the way ovarian cancer is treated and detected.

- Ovarian cancer treatment is being transformed with the arrival of customized medicine and targeted therapy.

Industry Trends and Drivers:

- Advancements in Diagnostic Techniques:

Innovations in diagnostic techniques are transforming ovarian cancer detection and treatment. Improved imaging technologies, such as transvaginal ultrasound and magnetic resonance imaging (MRI), allow for earlier and more accurate detection. In addition, advancements in biomarker research enable the identification of specific genetic mutations associated with ovarian cancer, leading to personalized treatment plans. Early detection is crucial for better prognosis and survival rates, thereby increasing the demand for advanced diagnostic tools. These innovations improve patient outcomes and encourage the development of new diagnostic products and technologies.

- Innovative Treatment Options:

The development of innovative treatment options, including targeted therapies and personalized medicine, is revolutionizing ovarian cancer care. Targeted therapies, such as poly (ADP-ribose) polymerase (PARP) inhibitors, specifically attack cancer cells with minimal impact on healthy cells and reduce side effects while improving efficacy. Personalized medicine tailors treatment to individual genetic profiles, enhancing effectiveness. Besides this, immunotherapy is emerging as a promising approach, leveraging the body's immune system to combat cancer. These advancements are leading to better patient outcomes, increased survival rates, and enhanced quality of life.

- Increasing Research and Development (R&D) Investments:

Pharmaceutical companies and research institutions are dedicating resources to discovering new treatments and improving existing therapies. These investments support extensive clinical trials, leading to the development of innovative drugs and advanced treatment modalities. R&D efforts focus on understanding the molecular mechanisms of ovarian cancer, identifying new drug targets, and optimizing treatment protocols. The continuous influx of funding accelerates the pace of scientific breakthroughs, bringing novel therapies to market faster. This commitment to R&D fosters a dynamic and competitive market landscape and offers hope for better patient outcomes.

Grab a sample PDF of this report: https://www.imarcgroup.com/ovarian-cancer-market/requestsample

Ovarian Cancer Market Report Segmentation:

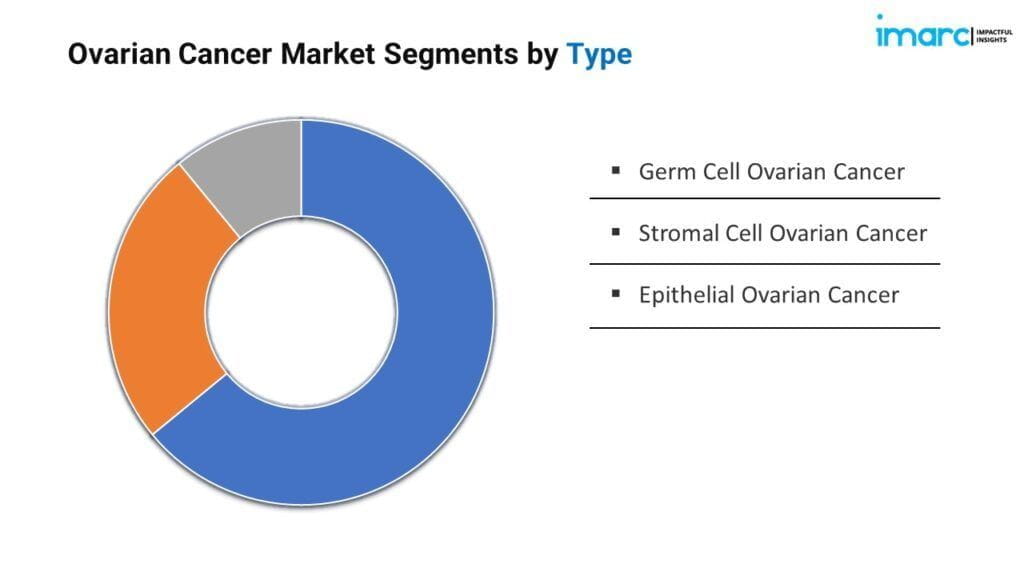

By Type:

- Epithelial Ovarian Cancer

- Germ Cell Ovarian Cancer

- Stromal Cell Ovarian Cancer

Epithelial ovarian cancer represents the largest segment as it is commonly diagnosed in older women.

By End User:

- Hospitals

- Homecare

- Speciality Centre

- Others

On the basis of the end user, the market has been divided into hospitals, homecare, speciality centre, and others.

Regional Insights:

- North America (United States, Canada)

- Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, Others)

- Europe (Germany, France, United Kingdom, Italy, Spain, Russia, Others)

- Latin America (Brazil, Mexico, Others)

- Middle East and Africa

North America enjoys a leading position in the ovarian cancer market on account of the presence of well-established and technologically advanced healthcare infrastructure.

Top Ovarian Cancer Market Leaders:

The ovarian cancer market research report outlines a detailed analysis of the competitive landscape, offering in-depth profiles of major companies. Some of the key players in the market are:

- AbbVie Inc.

- Amneal Pharmaceuticals Inc.

- AstraZeneca plc

- Eli Lilly and Company

- F. Hoffmann-La

- Roche AG

- GSK plc

- Hikma Pharmaceuticals PLC

- Lupin Limited

- Pfizer Inc.

- Teva Pharmaceutical Industries Ltd.

If you require any specific information that is not covered currently within the scope of the report, we will provide the same as a part of the customization.

About Us:

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provide a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: [email protected]

Tel No:(D) +91 120 433 0800

United States: +1-631-791-1145