stanley_imarc's blog

Global Surgical Equipment Market Statistics: USD 34.0 Billion Value by 2033

Summary:

- The global surgical equipment market size reached USD 19.9 Billion in 2024.

- The market is expected to reach USD 34.0 Billion by 2033, exhibiting a growth rate (CAGR) of 6.05% during 2025-2033.

- Asia Pacific leads the market, accounting for the largest surgical equipment market share.

- Reusable surgical equipment holds the biggest market share due to the cost-effectiveness and sustainability associated with these products.

- Hospitals account for the majority of the market share, attributed to their consistent need for surgical equipment and procedures.

- The increasing emergence of ambulatory surgical centers (ASCs) represents one of the crucial factors impelling the market growth.

- Rising advancements in technologies like robotic surgery, laser technology, and minimally invasive (MI) surgical instruments are contributing to the market growth.

Industry Trends and Drivers:

Factors Affecting the Growth of the Surgical Equipment Industry:

- Increase in Ambulatory Surgical Centers:

Ambulatory surgical centers (ASCs) experience expanding operations. ASCs provide patients better pricing structure along with simplified procedures compared to traditional hospital facilities. Patients experience shorter waiting periods and less infections and pay fewer costs at ASCs. The market depends heavily on this increasing trend. ASCs require an increased number of specialized surgical tools primarily for three areas involving eye care alongside orthopedics and digestive health procedures. The growth of ASCs leads to surgical care changes that in turn boost the need for customized surgical equipment.

- Rise in Surgical Procedures:

Healthcare access improvements along with better diagnostic tests combined with increasing patient numbers lead to an elevated surgical procedure rate across the world. The market benefits from this rising development. Additional healthcare infrastructure investments together with healthcare reimbursements are enabling more patients to undergo surgery. Public understanding about surgical procedures together with their associated benefits is now better understood. The increasing level of support helps grow market demand. Expanding surgical practice requires a greater amount of surgical equipment. Medical service providers are actively seeking out present-day advanced and efficient medical tools.

- Technological Advancements:

The surgery market expands because of robotic systems laser technology along with minimally invasive tools. The innovations introduce advantages that help doctors perform surgeries with higher accuracy along with reduced trauma to patients combined with quicker recovery times and better treatment results. Medical robots enhance surgeon control throughout intricate medical interventions. Through artificial intelligence along with machine learning healthcare providers achieve personalized treatment strategies with enhanced therapeutic effectiveness. The market shows positive signs for its bright future because of this growing trend.

Request for a sample copy of this report: https://www.imarcgroup.com/surgical-equipment-market/requestsample

Surgical Equipment Market Report Segmentation:

By Product:

- Surgical Sutures and Staplers

- Handheld Surgical Equipment

- Forceps and Spatulas

- Retractors

- Dilators

- Graspers

- Auxiliary Instruments

- Cutter Instruments

- Electrosurgical Devices

- Others

Surgical sutures and staplers represent the largest segment, thanks to their wide use and vital role in various surgical procedures.

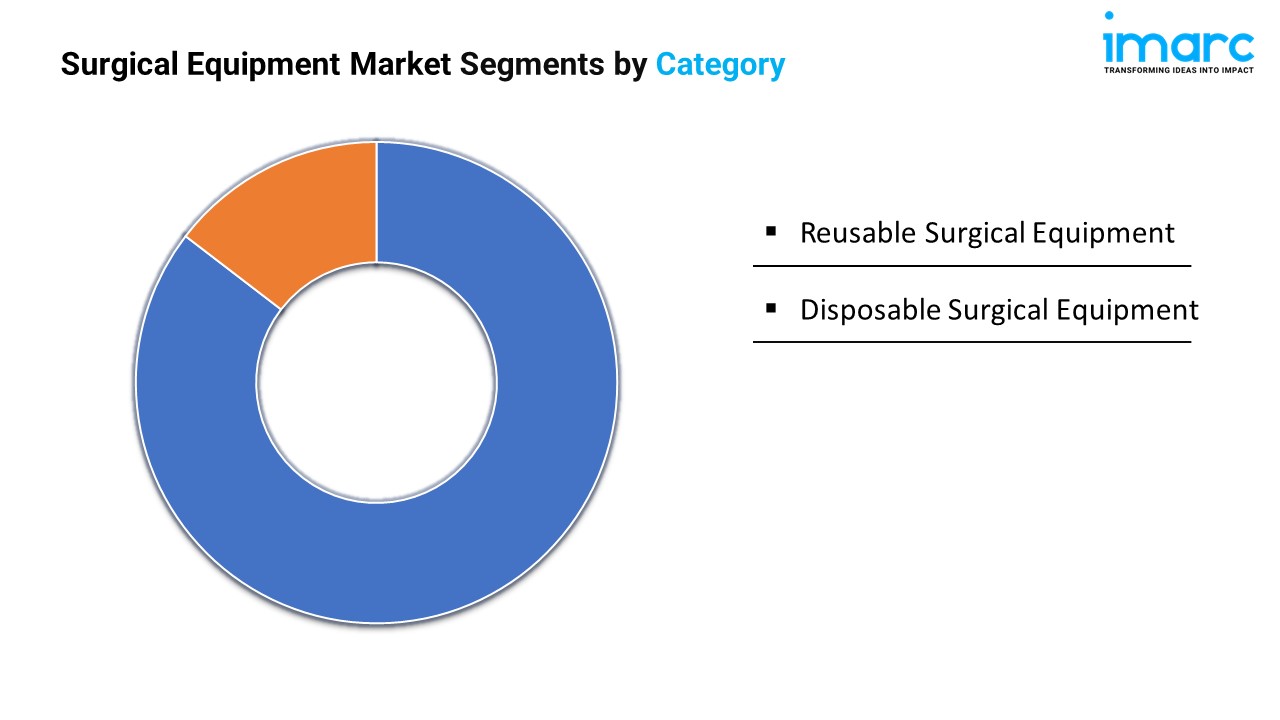

By Category:

- Reusable Surgical Equipment

- Disposable Surgical Equipment

Reusable surgical instruments hold the largest market share owing to the cost-effectiveness and durability associated with these products.

By Application:

- Neurosurgery

- Plastic and Reconstructive Surgery

- Wound Closure

- Obstetrics and Gynecology

- Cardiovascular

- Orthopedic

- Others

Based on application, the market has been segmented into neurosurgery, plastic and reconstructive surgery, wound closure, obstetrics and gynecology, cardiovascular, orthopedics, and others.

By End User:

- Hospitals

- Ambulatory Surgical Centers

- Others

Hospitals account for the majority of the market, owing to their constant need for surgical equipment and procedures.

Regional Insights:

- North America (United States, Canada)

- Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, Others)

- Europe (Germany, France, United Kingdom, Italy, Spain, Russia, Others)

- Latin America (Brazil, Mexico, Others)

- Middle East and Africa

North America dominates the market on account of its advanced healthcare infrastructure and a rising number of surgical procedures performed in the region.

Top Surgical Equipment Market Leaders:

The surgical equipment market research report outlines a detailed analysis of the competitive landscape, offering in-depth profiles of major companies. Some of the key players in the market are:

- Alcon

- B. Braun Melsungen AG

- Becton Dickinson and Company

- Boston Scientific Corporation

- CONMED Corporation

- Integra LifeSciences

- Intuitive Surgical Inc.

- Johnson & Johnson

- Medtronic plc

- Olympus Corporation

- Smith & Nephew plc

- Stryker Corporation

- Zimmer Biomet

Note: If you require any specific information that is not covered currently within the scope of the report, we will provide the same as a part of the customization.

About Us:

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provide a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: [email protected]

Tel No:(D) +91 120 433 0800

United States: +1-631-791-1145

IMARC Group’s report titled “Thermal Spray Coating Market Report by Product (Metals, Ceramics, Intermetallics, Polymers, Carbides, Abradables, and Others), Technology (Cold, Flame, Plasma, High-Velocity Oxy-Fuel (HVOF), Electric Arc, and Others), Application (Aerospace, Industrial Gas Turbine, Automotive, Medical, Printing, Oil and Gas, Steel, Pulp and Paper, and Others), and Region 2025-2033”. offers a comprehensive analysis of the industry, which comprises insights on the global thermal spray coating market share. The global market size reached USD 10.3 Billion in 2024. Looking forward, IMARC Group expects the market to reach USD 16.8 Billion by 2033, exhibiting a growth rate (CAGR) of 6.32% during 2025-2033.

Factors Affecting the Growth of the Thermal Spray Coating Industry:

- Demand for Thermal Sprays in the Aerospace Industry:

Thermal spray coatings experience market growth due to the aerospace industry. Thermal spray coatings serve as vital components used by aircraft producers to improve system durability and operational excellence. Engineering coatings serve as shield against wear damage as well as protection against both corrosion and high temperatures. Aerospace operations highly depend on these protective measures. The growing commercial aviation market and military spending also drive demand. These sectors share the common goal of achieving better efficiency together with longer-lasting aircraft service. Heavy pressure to reduce environmental impact results in new technological developments. The new innovations produce improvements in engine fuel consumption.

- Technological Advancements in Thermal Spray Processes:

Market growth receives an upward boost from continuously improving thermal spray technologies. Novel materials alongside modern equipment with novel methods now make the application of thermal spray more widespread. Advanced control systems along with automated production standards generate superior coating precision and reliability in core industrial operations. Scientists behind materials science perform research to create high-performance coatings which are effective in extreme operating environments. The industrial efficiency and affordability of thermal spray processes have increased through recent developments which drive companies from different sectors to integrate them into their operations.

- Demand for Corrosion and Wear Resistance in Industrial Applications:

Thermal spray coating demand expands rapidly throughout the oil, gas, power and chemical sectors. The three principal issues which these sectors deal with include both high heat exposure and corrosion alongside abrasion damage. Thermal spray coatings act as protective coverings which enhance equipment durability while decreasing operational expenses. Rising efficiency requirements drive the market increase for such coatings because of their need for reliability.

Grab a sample PDF of this report: https://www.imarcgroup.com/thermal-spray-coating-market/requestsample

Leading Companies Operating in the Global Thermal Spray Coating Industry:

- Air Products and Chemicals Inc.

- American Roller Company LLC

- Durum Verschleißschutz GmbH

- Lincotek Rubbiano S.p.A

- Metallizing Equipment Co. Pvt. Ltd.

- Montreal Carbide Co. Ltd.

- Powder Alloy Corporation

- Praxair Surface Technologies Inc. (Linde plc)

- Progressive Surface Inc.

- Wall Colmonoy Corporation

Thermal Spray Coating Market Report Segmentation:

By Product:

- Metals

- Ceramics

- Intermetallics

- Polymers

- Carbides

- Abradables

- Others

Ceramics exhibit a clear dominance in the market due to their excellent thermal and wear resistance properties.

By Technology:

- Cold

- Flame

- Plasma

- High-Velocity Oxy-Fuel (HVOF)

- Electric Arc

- Others

Plasma accounts for the majority of the market share as it provides precise and high-quality coatings.

By Application:

- Aerospace

- Industrial Gas Turbine

- Automotive

- Medical

- Printing

- Oil and Gas

- Steel

- Pulp and Paper

- Others

Aerospace represents the largest segment on account of the growing reliance on thermal spray coatings to enhance component durability and performance.

Regional Insights:

- North America (United States, Canada)

- Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, Others)

- Europe (Germany, France, United Kingdom, Italy, Spain, Russia, Others)

- Latin America (Brazil, Mexico, Others)

- Middle East and Africa

North America dominates the market, attributed to technological advancements and the increasing demand for thermal spray coatings across various sectors in the region.

Global Thermal Spray Coating Market Trends:

New environmental regulations are boosting market growth. These regulations aim to reduce VOC emissions and hazardous waste. They motivate industries to adopt environmentally friendly coatings. Thermal spray coatings, which are solvent-free, meet these regulations. This support promotes a shift from conventional to thermal spray coatings. It also promotes research and development for sustainable materials and processes. This trend is stronger in regions with strict environmental regulations.

Note: If you need specific information that is not currently within the scope of the report, we will provide it to you as a part of the customization.

About Us

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provide a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact US

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: [email protected]

Tel No:(D) +91 120 433 0800

United States: +1–631–791–1145

IMARC Group’s report titled “Insect Growth Regulators Market Report by Product (Chitin Synthesis Inhibitors, Juvenile Hormone Analogs and Mimics, Ecdysone Antagonists, Ecdysone Agonists), Form (Aerosol, Liquid, Bait), Application (Agriculture, Residential, Commercial), and Region 2025-2033” offers a comprehensive analysis of the industry, which comprises insights on the global insect growth regulators market share. The global market size reached USD 1,082.4 Million in 2024. Looking forward, IMARC Group expects the market to reach USD 1,768.2 Million by 2033, exhibiting a growth rate (CAGR) of 5.32% during 2025-2033.

Factors Affecting the Growth of the Insect Growth Regulators Industry:

- Environmental Concerns and Regulatory Policies:

Growing environmental concerns and strict regulatory policies aimed at reducing the use of conventional chemical pesticides are positively influencing the market. Insect growth regulators (IGRs) are being preferred over conventional pesticides as they are more targeted and less toxic to non-target species, including humans. This shift is a result of growing awareness about the adverse effects of chemical pesticides on the environment, which cause ecosystem imbalances and health hazards. Regulatory bodies around the world are imposing strict regulations on the use of pesticides, encouraging the adoption of eco-friendly alternatives. IGRs, which inhibit the growth and reproduction of pests without harming other organisms, are well aligned with these regulatory policies and environmental sustainability goals.

- Advancements in Agricultural Practices:

The adoption of modern and sustainable agricultural practices is driving the market growth. With the rise in global population, there is a tremendous need to enhance agricultural productivity while minimizing environmental impact. IGRs that provide sustainable solutions for pest management are becoming an integral part of integrated pest management (IPM) programmers. These substances work by disrupting the life cycle of pests, thereby controlling them without affecting crop yield. As farmers and agronomists are looking for innovative, effective and environmentally friendly ways to increase crop production and prevent pests, the demand for IGRs is increasing.

- Rising Demand for Organic Products:

Preferences for organic and naturally produced foods driven by concerns over food safety and the health implications of consuming products treated with synthetic chemicals are supporting the market growth. This shift is driving the demand for pest management solutions that are in line with organic farming standards, where IGRs play a vital role. Unlike conventional pesticides, IGRs are considered more compatible with organic agriculture due to their specific mode of action and low toxicity profile.

Request For Sample Copy of Report: https://www.imarcgroup.com/insect-growth-regulators-market/requestsample

Leading Companies Operating in the Global insect growth regulators Industry:

- BASF SE

- Central Life Science (Central Garden & Pet Company)

- Control Solutions Inc (China National Chemical Corporation)

- Dow Inc

- Nufarm Limited

- OHP Inc. (AMVAC Chemical Corporation)

- Russell IPM Ltd

- Sumitomo Chemical Co. Ltd. and Syngenta AG.

Insect Growth Regulators Market Report Segmentation:

By Product:

- Chitin Synthesis Inhibitors

- Juvenile Hormone Analogs and Mimics

- Ecdysone Antagonists

- Ecdysone Agonists

Chitin synthesis inhibitors represent the largest segment as they play a crucial role in pest management strategies across various industries.

By Form:

- Aerosol

- Liquid

- Bait

Liquid accounts for the majority of the market share due to their easy application.

By Application:

- Agriculture

- Residential

- Commercial

Agriculture exhibits a clear dominance in the market owing to the rising utilization of insect growth regulators in improving farming practices.

Regional Insights:

- North America (United States, Canada)

- Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, Others)

- Europe (Germany, France, United Kingdom, Italy, Spain, Russia, Others)

- Latin America (Brazil, Mexico, Others)

- Middle East and Africa

North America's dominance in the insect growth regulators market is attributed to investment in research and development (R&D), leading to the production of advanced insect growth regulators.

Global Insect Growth Regulators Market Trends:

The market for insect growth regulators is expanding rapidly due to three major factors, including advancements in technology and environmental sensitivity initiatives along with the developing needs for urban pest management. A growing number of agricultural actors and consumers choose sustainable practices, dramatically increasing the adoption of IGRs as a suitable pesticide alternative compared to conventional options. Product development and distribution advancements revolutionize the efficacy and safety profile of IGRs, stimulating farmer and pest management professional interest. Urbanization patterns create an even greater need for effective pest management tools, leading scientists to recognize insect growth regulators as basic tools for pest control of urban populations. The insect growth regulators market exhibits substantial expansion potential due to the growing industry momentum that supports sustainable pest control methods.

About Us

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provide a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact US

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: [email protected]

Tel No:(D) +91 120 433 0800

United States: +1-631-791-1145

Global Microcontroller Socket Industry: Key Statistics and Insights in 2025-2033

Summary:

- The global microcontroller socket market size reached USD 1.3 Billion in 2024.

- The market is expected to reach USD 1.9 Billion by 2033, exhibiting a growth rate (CAGR) of 4.54% during 2025-2033.

- Asia Pacific leads the market, accounting for the largest microcontroller socket market share.

- DIP accounts for the majority of the market share in the product segment, as DIP sockets provide reliable and secure connections, enhancing their usage in educational and industrial applications.

- Automotive holds the largest share in the microcontroller socket industry.

- The rising demand for electronic devices is a primary driver of the microcontroller socket market.

- Technological advancements and the integration of smart home technologies are reshaping the microcontroller socket market.

Request for a sample copy of this report: https://www.imarcgroup.com/microcontroller-socket-market/requestsample

Industry Trends and Drivers:

- Rising demand for electronic devices:

Smartphones, tablets, laptops, smart TVs, and other gadgets are promoting the use of microcontroller sockets. These sockets are essential for device operation. Microcontrollers enable functionality within these electronics. Additionally, more devices are connecting to the Internet, creating new ways to control our environment. Examples include smart heating systems, fitness-monitoring wristbands, and smart home appliances. All of these IoT devices rely on microcontroller sockets for effective communication and management. In addition, these sockets are critical for automating manufacturing, robotics, and control systems.

Technological advancements in microcontroller technology:

Today microcontrollers are more advanced and complex. They handle multiple calculations and functions. This advancement requires new sockets that can support these next-generation microcontrollers. Such sockets help them realize their full potential. There has also been a rise in low-power microcontrollers, especially for portable devices and IoT. As energy efficiency improves, the need for sockets that work with these energy-saving microcontrollers also grows. Additionally, modern microcontrollers have more interfacing features such as Bluetooth, Wi-Fi, and cellular connectivity. This increase in features creates a demand for sockets with additional pins and interfaces, making connectivity easier.

Environmental regulations:

New policies such as RoHS and REACH require manufacturers to reduce hazardous substances in microcontroller sockets. Major manufacturers demand compliant designs and materials. They focus on producing sockets free of restricted substances. Additionally, their goal is to increase the life of the device. This leads to the production of more robust sockets. These sockets can last as long as the device itself. By doing this, manufacturers help reduce waste and e-waste.

We explore the factors driving the growth of the market, including technological advancements, consumer behaviors, and regulatory changes, along with emerging microcontroller socket market trends.

Microcontroller Socket Market Report Segmentation:

Breakup By Product:

- DIP

- BGA

- QFP

- SOP

- SOIC

DIP represents the largest segment due to its widespread use in various electronic applications and compatibility with a wide range of microcontrollers.

Breakup By Application:

- Automotive

- Consumer Electronics

- Industrial

- Medical Devices

- Military and Defense

Automotive accounted for the largest market share on account of the increasing integration of microcontrollers in modern vehicles, controlling various functions, ranging from engine management to infotainment systems.

Breakup By Region:

- North America (United States, Canada)

- Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, Others)

- Europe (Germany, France, United Kingdom, Italy, Spain, Russia, Others)

- Latin America (Brazil, Mexico, Others)

- Middle East and Africa

Asia Pacific’s dominance in the microcontroller socket market is attributed to the rising production of electronic devices and appliances that require microcontroller sockets.

Top Microcontroller Socket Market Leaders:

The microcontroller socket market research report outlines a detailed analysis of the competitive landscape, offering in-depth profiles of major companies. Some of the key players in the market are:

- Advanced Interconnections

- Andon Electronics

- Aries Electronics Inc.

- Johnstech International Corporation

- Loranger International Corporation

- Microchip Technology

- Mill-Max Mfg. Corp.

- PRECI-DIP SA

- TE Connectivity

- Texas Instruments Inc.

Note: If you require any specific information that is not covered currently within the scope of the report, we will provide the same as a part of the customization.

About Us

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provide a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact US

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: [email protected]

Tel No:(D) +91 120 433 0800

United States: +1–631–791–1145

IMARC Group’s report titled “Endoscopic Retrograde Cholangiopancreatography Market Report by Product (Endoscope, Endotherapy Devices, Visualization Systems, Energy Devices, and Others), Procedure (Biliary Sphincterotomy, Biliary Stenting, Biliary Dilatation, Pancreatic Sphincterotomy, Pancreatic Duct Stenting, Pancreatic Duct Dilatation), End User (Hospitals and Clinics, Ambulatory Surgery Centers, and Others), and Region 2025-2033”. offers a comprehensive analysis of the industry, which comprises insights on the global endoscopic retrograde cholangiopancreatography market share. The global market size reached USD 1.7 Billion in 2024. Looking forward, IMARC Group expects the market to reach USD 2.8 Billion by 2033, exhibiting a growth rate (CAGR) of 5.58% during 2025-2033.

Factors Affecting the Growth of the Endoscopic Retrograde Cholangiopancreatography Industry:

- Increasing Prevalence of Gastrointestinal Diseases:

Whereas the increasing global population is suffering from GI diseases makes the demand for ERCP growing correspondingly. Illnesses, for instance, cholelithiasis, pancreatitis and bile stones are on the Rise due to poor diet, obesity and inadequate physical activity. These diseases entail tricky diagnosis and treatment procedures that are offered by ERCP. Besides this, many other chronic diseases requiring frequent surveillance and management including inflammatory bowel disease (IBD) and chronic pancreatitis where ERCP is very useful.

- Advancements in Technology:

Enhanced visualisation modalities include high definition endoscopy which facilitate better diagnosis of biliary and pancreatic pathologies as well as forward and reverse imaging fluroscopy. Techniques of ERCP such as the minimally invasive (MI) ones enable the patient’s recovery time to be shorter and the risks of complications to be lower than in other procedures, thus client and provider interest is increased. Better designs of stents and various extraction devices also in the field of endoscopy have broadened therapeutic roles of ERCP. Therefore, the process receives help in enhancing the efficiency and security supported by technologies.

- Rising Awareness and Diagnosis Rates:

The growth of public awareness as regards gastrointestinal diseases and the need for early diagnosis is also helping the market to grow. Public and health promotion and the overall availability of health care information has made more patient’s present with gastrointestinal symptoms at an earlier stage. Such an approach leads to early diagnosis of various ailments that can actually be cured or controlled through ERCP. Also, physicians and other healthcare workers are in a better position and more sensitive to prescribe ERCP when initial outpatient tests suggest biliary or pancreatic pathology.

Grab a sample PDF of this report: https://www.imarcgroup.com/endoscopic-retrograde-cholangiopancreatography-market/requestsample

Leading Companies Operating in the Endoscopic Retrograde Cholangiopancreatography Industry:

- Boston Scientific Corporation

- CONMED Corporation

- Cook Group Incorporated

- Fujifilm Holdings Corporation

- Hobbs Medical Inc.

- Johnson & Johnson

- Medi-Globe GmbH

- Medtronic plc

- Olympus Corporation

- Shaili Endoscopy

- Steris Corporation and Telemed Systems Inc.

Endoscopic Retrograde Cholangiopancreatography Market Report Segmentation:

By Product:

- Endoscope

- Endotherapy Devices

- Sphincterotomes

- Lithotripter

- Stents

- Visualization Systems

- Energy Devices

- Others

Endotherapy devices represent the largest segment as they are crucial for both diagnostic and therapeutic purposes.

By Procedure:

- Biliary Sphincterotomy

- Biliary Stenting

- Biliary Dilatation

- Pancreatic Sphincterotomy

- Pancreatic Duct Stenting

- Pancreatic Duct Dilatation

Biliary sphincterotomy holds the biggest market share due to the rising prevalence of biliary conditions among individuals.

By End User:

- Hospitals and Clinics

- Ambulatory Surgery Centers

- Others

Hospitals and clinics account for the largest market share, driven by their ability to provide comprehensive healthcare services.

Regional Insights:

- North America (the United States and Canada)

- Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, and others)

- Europe (Germany, France, the United Kingdom, Italy, Spain, and others)

- Latin America (Brazil, Mexico, and others)

- Middle East and Africa.

North America enjoys a leading position in the endoscopic retrograde cholangiopancreatography market on account of the presence of highly developed healthcare infrastructure.

Global Endoscopic Retrograde Cholangiopancreatography Market Trends:

Age-related conditions such as gallstones, pancreatic cancer, and biliary strictures are common in the elderly, requiring frequent diagnostic and therapeutic interventions. Older people often require comprehensive and less invasive treatment options, making ERCP a preferred option because of its ability to combine diagnosis and treatment in a single procedure.

Collaborations between key market players, healthcare providers, and research institutions are driving the development of new products and technologies. In addition, ERCP is increasingly being used for therapeutic purposes, such as stent placement, stone removal, and tissue sampling, contributing to market growth. It can perform combined diagnostic and therapeutic procedures in a single session.

Note: If you need specific information that is not currently within the scope of the report, we will provide it to you as a part of the customization.

About Us

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provide a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact US

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: [email protected]

Tel No:(D) +91 120 433 0800

United States: +1–631–791–1145

IMARC Group’s report titled “Collagen Supplement Market Report by Source (Marine and Poultry, Porcine, Bovine), Product (Gelatin Collagen Supplements, Hydrolyzed Collagen Supplements, Native Collagen Supplements), Form (Pills and Gummies, Powder, Liquid/Drinks), Sales Channel (Pharmacy, Specialty Store, Online Store), Application (Nutraceuticals, Cosmetics, Healthcare, Food, and Others), and Region 2025-2033”. The global collagen supplement market size reached USD 2.4 Billion in 2024. Looking forward, IMARC Group expects the market to reach USD 3.5 Billion by 2033, exhibiting a growth rate (CAGR) of 4.17% during 2025-2033.

Factors Affecting the Growth of the Collagen Supplement Industry:

● Aging Population:

Collagen is a crucial component of the skin, providing structure, elasticity, and hydration. As people age, their natural collagen production decreases, leading to wrinkles, sagging skin, and other signs of aging. Older individuals are increasingly seeking ways to maintain a youthful appearance, and collagen supplements are marketed as effective solutions for improving skin elasticity and reducing wrinkles. Aging often brings joint-related issues, such as arthritis and reduced mobility, due to the degradation of cartilage, which is largely composed of collagen. Collagen supplements are promoted for their potential to support joint health, reduce pain, and improve mobility, making them appealing to older adults looking to maintain an active lifestyle.

● Health and Wellness Trends:

Modern consumers are adopting a holistic approach to health, emphasizing the importance of overall well-being rather than just treating specific conditions. Collagen supplements, which offer benefits for skin, hair, nails, joints, and gut health, align well with this comprehensive health focus. There is a growing trend of beauty from within solutions, where people prefer dietary supplements that enhance beauty naturally from the inside out. Collagen supplements are widely marketed for their ability to improve skin elasticity, hydration, and reduce wrinkles, fitting perfectly into this trend.

● Product Innovations:

Collagen supplements are now available in multiple forms, including powders, capsules, gummies, liquids, and even ready-to-drink beverages. This variety caters to different consumer preferences, making it easier for people to incorporate collagen into their daily routines. Innovations in formulation have led to the development of collagen peptides and hydrolyzed collagen, which are more easily absorbed by the body. This improved bioavailability increases the effectiveness of the supplements, encouraging more consumers to use them.

Grab a sample PDF of this report: https://www.imarcgroup.com/collagen-supplement-market/requestsample

Leading Companies Operating in the Global Collagen Supplement Industry:

- Absolute Collagen

- BioTech USA Ltd.

- Codeage LLC, Further Inc.

- Hunter and Gather Foods

- Nestlé S.A.

- Nutraformis Limited

- Optimum Nutrition (Glanbia Performance Nutrition India Pvt. Ltd)

- Proto-col

- Revive Collagen

- Shiseido Company Limited

- TCI Co. Ltd.

- The Clorox Company.

Collagen Supplement Market Report Segmentation:

By Source:

- Marine and Poultry

- Porcine

- Bovine

Bovine represents the largest segment due to its high availability, cost-effectiveness, and well-established benefits for joint and skin health.

By Product:

- Gelatin Collagen Supplements

- Hydrolyzed Collagen Supplements

- Native Collagen Supplements

Gelatin collagen supplements account for the majority of the market share because they are versatile, easily digestible, and cost-effective, making them a staple in the market.

By Form:

- Pills and Gummies

- Powder

- Liquid/Drinks

Pills and gummies exhibit a clear dominance in the market as they are favored for their convenience and ease of consumption, appealing to a broad range of consumers.

By Sales Channel:

- Pharmacy

- Specialty Store

- Online Store

Pharmacy holds the biggest market share owing to its accessibility and the trust consumers place in them for health-related products.

By Application:

- Nutraceuticals

- Cosmetics

- Healthcare

- Food

- Others

Healthcare dominates the market. Collagen supplements are primarily used in healthcare applications to support skin, joint, and bone health, driving their dominance in the market.

Regional Insights:

- North America (United States, Canada)

- Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, Others)

- Europe (Germany, France, United Kingdom, Italy, Spain, Russia, Others)

- Latin America (Brazil, Mexico, Others)

- Middle East and Africa

North America enjoys the leading position in the collagen supplement market on account of its high consumer awareness, advanced healthcare infrastructure, and a strong focus on health and wellness trends.

Global Collagen Supplement Market Trends:

There is increasing consumer interest in supplements that promote skin health, reduce wrinkles, and enhance overall appearance from the inside out. Tailored collagen supplements that address specific health needs, such as joint support or gut health, are gaining traction as consumers are seeking customized wellness solutions. New product forms, including gummies, liquid shots, and functional beverages, are becoming more prevalent, offering convenience and enhancing consumer appeal. There is a growing emphasis on ethically and sustainably sourced collagen, such as marine or grass-fed bovine collagen, reflecting consumer concerns about environmental impact and animal welfare.

Note: If you need specific information that is not currently within the scope of the report, we will provide it to you as a part of the customization.

About Us

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provide a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact US

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: [email protected]

Tel No:(D) +91 120 433 0800

United States: +1–631–791–1145

Global Tag Management System Industry: Key Statistics and Insights in 2025-2033

Summary:

- The global tag management system market size reached USD 1,150 Million in 2024.

- The market is expected to reach USD 2,909.7 Million by 2033, exhibiting a growth rate (CAGR) of 10.9% during 2025-2033.

- North America leads the market, accounting for the largest tag management system market share.

- Tools account for the majority of the market share in the component segment.

- On-premises holds the largest share in the tag management system industry.

- Large enterprises remain a dominant segment in the market.

- IT and telecommunication represent the leading segment.

- The rise in demand for data-driven marketing and analysis is a primary driver of the tag management system market.

- The advent of stringent data protection regulations and other similar laws worldwide is reshaping the tag management system market.

Industry Trends and Drivers:

- Growing Demand for Data-Driven Marketing and Analytics:

At present, businesses are relying on data-driven marketing strategies to gain insights into customer behavior, optimize campaigns, and enhance decision-making processes. Tag management systems (TMS) play a crucial role in this landscape by efficiently deploying and managing various tracking tags that collect valuable data from websites and mobile applications. As companies seek to leverage big data and advanced analytics to stay competitive, the complexity of handling multiple tags from different vendors becomes a significant challenge. TMS solutions simplify this process by providing a centralized platform for tag deployment, reducing the need for constant developer intervention and minimizing errors. Furthermore, the ability to quickly implement and adjust tracking tags enables marketers to respond swiftly to changing market trends and consumer preferences.

- Need for Improved Website Performance and User Experience:

Website performance and user experience are critical factors that influence customer satisfaction, engagement, and conversion rates. The proliferation of various marketing and analytics tags can significantly slow down website loading times, leading to higher bounce rates and diminished user experiences. Tag management systems address this issue by optimizing the deployment and execution of tags, ensuring that they do not adversely affect site performance. By asynchronously loading tags and managing their firing sequences, TMS solutions help maintain fast page load speeds and seamless interactions for users. Additionally, TMS platforms often include features, such as tag prioritization, conditional loading, and performance monitoring, which further enhance website efficiency. As businesses recognize the direct correlation between website performance and their bottom line, the demand for tag management systems that can maintain optimal site functionality while supporting robust marketing initiatives is rising.

- Increasing Emphasis on Data Privacy and Regulatory Compliance:

With the advent of stringent data protection regulations and other similar laws worldwide, businesses are under heightened pressure to ensure compliance in their data collection and processing activities. TMS is instrumental in assisting organizations to manage and control the deployment of tracking tags in a manner that adheres to these regulations. TMS solutions offer features, such as consent management, data anonymization, and granular control over which tags are activated based on user permissions. By centralizing tag governance, companies can more easily implement and enforce privacy policies, reduce the risk of non-compliance penalties, and build trust with their customers. Additionally, the ability to audit and document tag activities is essential for regulatory reporting and accountability.

Request for a sample copy of this report: https://www.imarcgroup.com/tag-management-system-market/requestsample

Tag Management System Market Report Segmentation:

Breakup By Component:

- Tools

- Service

Tools exhibit a clear dominance in the market as businesses prioritize comprehensive solutions that enable efficient deployment, monitoring, and optimization of multiple tracking tags without requiring extensive technical resources.

Breakup By Deployment Model:

- On-premises

- Cloud-based

On-premises represent the largest segment because organizations prefer the enhanced security, customization, and control it offers over their tag management systems, ensuring data sovereignty and tailored configurations.

Breakup By Organization Size:

- Small and Medium-sized Enterprises

- Large Enterprises

Large enterprises hold the biggest market share due to their extensive digital operations, complex tagging requirements, and greater investment capabilities in advanced tag management solutions to support their expansive marketing and analytics initiatives.

Breakup By Industry Vertical:

- Healthcare

- Retail and e-commerce

- BFSI

- IT and Telecommunication

- Media and Entertainment

- Manufacturing

- Others

IT and telecommunication account for the majority of the market share since these industries extensively utilize tag management systems to handle vast amounts of data, optimize digital marketing strategies, and ensure seamless integration across diverse digital platforms.

Breakup By Region:

- North America (United States, Canada)

- Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, Others)

- Europe (Germany, France, United Kingdom, Italy, Spain, Russia, Others)

- Latin America (Brazil, Mexico, Others)

- Middle East and Africa

North America dominates the market owing to stringent data privacy regulations, driving organizations to adopt sophisticated tag management systems to ensure compliance, secure data handling, and maintain trust.

Top Tag Management System Market Leaders:

The tag management system market research report outlines a detailed analysis of the competitive landscape, offering in-depth profiles of major companies. Some of the key players in the market are:

- Adform

- Adobe Inc.

- Blue Triangle Technologies Inc.

- Commanders Act

- Ensighten Inc.

- Google LLC (Alphabet Inc.)

- International Business Machines Corporation

- Observepoint Inc.

- Oracle Corporation

- Relay42 Netherlands B.V.

- Segment.io Inc. (Twilio)

- Tealium Inc.

Note: If you require any specific information that is not covered currently within the scope of the report, we will provide the same as a part of the customization.

About Us:

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provide a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: [email protected]

Tel No:(D) +91 120 433 0800

United States: +1–631–791–1145

Global Rosacea Treatment Industry: Key Statistics and Insights in 2025-2033

Summary:

- The global rosacea treatment market size reached USD 2.1 Billion in 2024.

- The market is expected to reach USD 3.3 Billion by 2033, exhibiting a growth rate (CAGR) of 5.3% during 2025-2033.

- North America leads the market, accounting for the largest rosacea treatment market share.

- On the basis of type, the market has been divided into erythematotelangiectatic rosacea, papulopustular rosacea, ocular rosacea, and phymatous rosacea.

- Antibiotics account for the majority of the market share in the drug class segment as they benefit in reducing redness, swelling, and bumps.

- Topical holds the largest share in the rosacea treatment industry.

- Based on the distribution channel, the market has been classified into hospital pharmacy, online pharmacy, retail pharmacy, and others.

- On the basis of end user, the market has been segmented into hospitals, homecare, specialty clinics, and others.

- The rising prevalence of rosacea is a primary driver of the rosacea treatment market.

- Technological advancements in treatment options and increasing awareness and dermatological consultations are reshaping the rosacea treatment market.

Rosacea Treatment Industry Trends and Drivers:

- Growing Prevalence of Rosacea:

The increasing prevalence of rosacea among people worldwide is fueling the market growth. Environmental factors, such as air pollution and poor weather conditions, combined with rising levels of stress and lifestyle changes are contributing to the development of rosacea symptoms. Rosacea is a chronic skin condition characterized by facial redness, inflammation, and visible blood vessels. As more individuals in both developed and developing regions are affected, the demand for treatment options is increasing. This trend is encouraging pharmaceutical companies and dermatologists to develop new treatment solutions, ranging from topical applications to systemic drugs, to meet the diverse needs of individuals.

- Rising Awareness and Dermatological Consultations:

Increasing awareness among people about the symptoms of rosacea and the importance of seeking medical advice is fueling the market growth. More people are recognizing rosacea at an early stage due to public health campaigns, social media discussions, and educational initiatives of dermatology societies. In addition, the increasing availability of dermatology consultations in both urban and rural areas is contributing to the market growth. Patients are willing to visit specialists and invest in treatments that reduce the appearance and discomfort of rosacea. There is an increase in demand for effective treatment options, such as topical creams, antibiotics, and laser therapy, as more people understand the triggers and actively manage the condition.

- Technological Advancements in Treatment Options:

Advanced therapies, such as pulsed dye laser (PDL) and intense pulsed light (IPL) treatments, are gaining popularity on account of their effectiveness in reducing redness and visible blood vessels associated with rosacea. Innovations in topical medications and oral drugs are also benefit in improving treatment outcomes for patients with different rosacea subtypes. Apart from this, non-invasive treatment options are becoming more accessible and are preferred by patients looking for minimal side effects and faster recovery times. As a result, these advancements are broadening the range of treatment options available in the market, making it easier for patients to find suitable therapies.

Request for a sample copy of this report: https://www.imarcgroup.com/rosacea-treatment-market/requestsample

Rosacea Treatment Market Report Segmentation:

Breakup By Type:

- Erythematotelangiectatic Rosacea

- Papulopustular Rosacea

- Ocular Rosacea

- Phymatous Rosacea

On the basis of type, the market has been divided into erythematotelangiectatic rosacea, papulopustular rosacea, ocular rosacea, and phymatous rosacea.

Breakup By Drug Class:

- Antibiotics

- Alpha Agonists

- Retinoids

- Corticosteroids

- Immunosuppressants

- Antihypertensive Agents

- Others

Antibiotics dominate the market as they benefit in reducing redness, swelling, and bumps.

Breakup By Route of Administration:

- Topical

- Oral

Topical represents the majority of shares due to the convenience of application and fewer long-term risks compared to oral treatments.

Breakup By Distribution Channel:

- Hospital Pharmacy

- Online Pharmacy

- Retail Pharmacy

- Others

Based on the distribution channel, the market has been classified into hospital pharmacy, online pharmacy, retail pharmacy, and others.

Breakup By End User:

- Hospitals

- Homecare

- Specialty Clinics

- Others

On the basis of end user, the market has been segmented into hospitals, homecare, specialty clinics, and others.

Breakup By Region:

- North America (United States, Canada)

- Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, Others)

- Europe (Germany, France, United Kingdom, Italy, Spain, Russia, Others)

- Latin America (Brazil, Mexico, Others)

- Middle East and Africa

North America enjoys the leading position owing to a large market for rosacea treatment driven by the presence of advanced healthcare infrastructure.

Top Rosacea Treatment Market Leaders:

The rosacea treatment market research report outlines a detailed analysis of the competitive landscape, offering in-depth profiles of major companies. Some of the key players in the market are:

- Bausch Health Companies Inc.

- Cellix Bio Private Limited

- Colorescience Inc.

- Croda International Plc

- Galderma S.A.

- LEO Pharma A/S

- Lupin Limited

- Maruho Co. Ltd.

- PruGen Pharmaceuticals, Sol-Gel Technologies Ltd.

- Timber Pharmaceuticals LLC.

Note: If you require any specific information that is not covered currently within the scope of the report, we will provide the same as a part of the customization.

About Us:

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provide a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: [email protected]

Tel No:(D) +91 120 433 0800

United States: +1-631-791-1145

Global Alpha Emitter Industry: Key Statistics and Insights in 2025-2033

Summary:

- The global alpha emitter market size reached USD 1,834.5 Million in 2024.

- The market is expected to reach USD 12,040.2 Million by 2033, exhibiting a growth rate (CAGR) of 23.25% during 2025-2033.

- North America leads the market, accounting for the largest alpha emitter market share.

- Ovarian cancer holds the biggest market share due to the rising need for effective and targeted therapies.

- On the basis of the end user, the market has been divided into hospitals, medical research institutions, and others.

- The rising prevalence of cancer among the masses across the globe is catalyzing the demand for alpha emitters.

- Technological advancements in radiopharmaceuticals are revolutionizing the field of nuclear medicine.

Industry Trends and Drivers:

- Increasing Prevalence of Cancer:

The rising prevalence of cancer among the masses across the globe is catalyzing the demand for alpha emitters. The growing need for advanced treatment options like targeted alpha-particle therapy (TAT) among individuals who are diagnosed with various types of cancer, especially those that are aggressive and difficult to treat with conventional therapies, is offering a favorable market outlook. Alpha emitters deliver high-energy particles directly to cancer cells with minimal impact on surrounding healthy tissues, making them crucial in the fight against cancer. This targeted approach is particularly effective for treating metastatic cancers and those that have developed resistance to traditional therapies.

- Advancements in Radiopharmaceuticals:

Technological advancements in radiopharmaceuticals are revolutionizing the field of nuclear medicine. Innovations in the development, production, and application of radiopharmaceuticals improve the efficacy, safety, and accessibility of alpha emitters in medical treatments. These advancements include better targeting mechanisms, enhanced imaging techniques, and the development of new isotopes that provide more effective treatment options. The ability to accurately deliver alpha emitters to cancer cells while minimizing damage to healthy tissues is making these therapies more appealing to both healthcare providers and patients. Furthermore, improvements in radiopharmaceutical production processes are leading to increased availability and reduced costs.

- Growing Demand for Targeted Therapy:

The shift towards personalized and targeted cancer therapies is supporting the market growth. Targeted therapy focuses on specific molecules or pathways that are involved in the growth and survival of cancer cells, offering a more precise treatment approach as compared to traditional chemotherapy or radiation. Alpha emitters play a crucial role in this therapeutic strategy by delivering potent radiation directly to cancer cells, thereby reducing collateral damage to healthy tissues. This precision is particularly important for treating cancers that are difficult to reach or have spread to multiple areas in the body.

Request for a sample copy of this report: https://www.imarcgroup.com/alpha-emitter-market/requestsample

Alpha Emitter Market Report Segmentation:

By Type of Radionuclide:

- Astatine

- Radium

- Actinium

- Lead

- Bismuth

- Others

Radium represents the largest segment as it is valued for its ability to emit high-energy alpha particles, which can effectively target and destroy cancer cells while minimizing damage to surrounding healthy tissue.

By Medical Application:

- Prostate Cancer

- Bone Metastasis

- Ovarian Cancer

- Pancreatic Cancer

- Endocrine Tumors

- Others

Ovarian cancer holds the biggest market share due to the rising need for effective and targeted therapies.

By End User:

- Hospitals

- Medical Research Institutions

- Others

On the basis of the end user, the market has been divided into hospitals, medical research institutions, and others.

Regional Insights:

- North America (United States, Canada)

- Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, Others)

- Europe (Germany, France, United Kingdom, Italy, Spain, Russia, Others)

- Latin America (Brazil, Mexico, Others)

- Middle East and Africa

North America enjoys a leading position in the alpha emitter market on account of the presence of highly advanced healthcare systems and research institutions.

Top Alpha Emitter Market Leaders:

The alpha emitter market research report outlines a detailed analysis of the competitive landscape, offering in-depth profiles of major companies. Some of the key players in the market are:

- Actinium Pharmaceuticals Inc.

- Alpha Tau Medical Ltd.

- Bayer AG

- Fusion Pharmaceuticals

- IBA RadioPharma Solutions

- RadioMedix Inc.

Note: If you require any specific information that is not covered currently within the scope of the report, we will provide the same as a part of the customization.

About Us:

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provide a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: [email protected]

Tel No:(D) +91 120 433 0800

United States: +1-631-791-1145

IMARC Group’s report titled "Distribution Transformer Market Report by Insulation Type (Dry, Liquid Immersed), Mounting (Pad, Pole, Underground vault), Phase (Single, Three), Power Rating (Up to 500 kVA, 501 kVA–2500 kVA, Above 2500 kVA), and Region 2025-2033". The global distribution transformer market size reached USD 21.1 Billion in 2024. Looking forward, IMARC Group expects the market to reach USD 31.4 Billion by 2033, exhibiting a growth rate (CAGR) of 4.32% during 2025-2033.

Factors Affecting the Growth of the Distribution Transformer Industry:

- Power Demand and Consumption:

The increasing demand for electricity in the industrial sector to operate various machines represents one of the crucial factors impelling the growth of the market. Besides this, infrastructure development is leading to the establishment of new residential and commercial areas. The creation of these spaces requires the installation of distribution transformers to supply power to the buildings and facilities. Distribution transformers are crucial components in the power distribution network, ensuring that the energy generated at power plants is efficiently delivered to industrial facilities. Apart from this, aging power infrastructure in many regions requires upgrades and modernization to enhance efficiency and reliability. This often involves the installation of new and more efficient distribution transformers to replace outdated ones and accommodate changing energy needs.

- Digital Transformation of Industries:

The ongoing digital transformation across industries is positively influencing the distribution transformer market. The integration of digital technologies, such as Internet of Things (IoT) sensors and communication systems, is enabling utilities to monitor and manage distribution transformers in real-time. This trend is contributing to the development of smart grids, where distribution transformers play a pivotal role in optimizing power distribution and enhancing grid intelligence. The adoption of digital solutions is not only improving operational efficiency but also facilitating predictive maintenance, reducing downtime, and extending the lifespan of distribution transformers.

- Smart Grid Implementation:

Smart grids enable better monitoring and control of energy distribution. This leads to more efficient use of electricity, reducing losses during transmission and distribution. As a result, there is a growing demand for distribution transformers that are compatible with smart grid technologies to maximize energy efficiency. Smart grids also allow utilities to monitor and control distribution transformers remotely. This capability enables real-time data collection, analysis, and predictive maintenance. Furthermore, distribution transformers equipped with smart sensors and communication capabilities are becoming crucial for efficient grid management.

Grab a sample PDF of this report: https://www.imarcgroup.com/distribution-transformer-market/requestsample

Leading Companies Operating in the Global Distribution Transformer Industry:

![]()

- CG Power and Industrial Solutions Limited (Murugappa Group)

- Eaton Corporation PLC

- EMCO Limited

- General Electric

- Hammond Power Solutions Inc.

- Hitachi Energy Ltd, Ormazabal (Velatia S.L.)

- Schneider Electric

- SGB-Smit Group

- Siemens AG

- Toshiba Energy Systems & Solutions Corporation (Toshiba Corporation)

- Wilson Power Solutions and Wilson Transformer Company.

Distribution Transformer Market Report Segmentation:

By Insulation Type:

- Dry

- Liquid Immersed

Liquid immersed is the most popular type as it is used to dissipate heat generated during the operation of the transformer and to provide insulation to prevent electrical breakdown.

By Mounting:

![]()

- Pad

- Pole

- Underground vault

Pad accounted for the largest market share due to its cost-effectiveness and convenience.

By Phase:

- Single

- Three

On the basis of the phase, the market has been segmented into single and three.

By Power Rating:

- Up to 500 kVA

- 501 kVA–2500 kVA

- Above 2500 kVA

Up to 500 kVA represents the maximum share as it is used for distributing electrical power from the utility grid to residential, commercial, and industrial areas.

Regional Insights:

- North America (United States, Canada)

- Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, Others)

- Europe (Germany, France, United Kingdom, Italy, Spain, Russia, Others)

- Latin America (Brazil, Mexico, Others)

- Middle East and Africa

Asia Pacific's dominance in the distribution transformer market is attributed to rising investments in electrification projects and increasing focus on reducing transmission losses by stepping down the voltage before the electricity is distributed over shorter distances.

Global Distribution Transformer Market Trends:

Government initiatives, regulations, and policies related to energy efficiency, grid reliability, and environmental standards can significantly impact the distribution transformer industry. Moreover, innovations in transformer design, materials, and manufacturing processes is contributing to the market growth.

The growing awareness of energy efficiency and the need to reduce energy losses in power distribution is leading to the development and adoption of more efficient distribution transformer technologies. Furthermore, the increasing awareness of environmental issues and the focus on reducing carbon emissions is leading to the adoption of environmentally friendly and energy-efficient distribution transformer technologies.

Note: If you need specific information that is not currently within the scope of the report, we will provide it to you as a part of the customization.

About Us

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provide a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact US

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: [email protected]

Tel No:(D) +91 120 433 0800

United States: +1-631-791-1145