sujeet123's blog

IMARC Group's report titled "Autonomous Vehicle Market Report by Component (Hardware, Software and Services), Level of Automation (Level 3, Level 4, Level 5), Application (Transportation and Logistics, Military and Defense), and Region 2024-2032". The global autonomous vehicle market size reached USD 109.0 Billion in 2024. Looking forward, IMARC Group expects the market to reach USD 1,730.4 Billion by 2033, exhibiting a growth rate(CAGR) of 31.85% during 2025-2033.

For an in-depth analysis, you can refer sample copy of the report: https://www.imarcgroup.com/autonomous-vehicle-market/requestsample

Factors Affecting the Growth of the Autonomous Vehicle Industry:

- Technological Advancements:

Progresses are on the innovations aspects in the development of the autonomous vehicle (AV). New improvements in AI and ML technologies can let AVs understand the extensive information flowing from the environment and respond instantly to optimize safety and efficacy. The administration coming from these techniques of sensors, including LIDAR, radar, and cameras, offers the right data for these types of algorithms to operate effectively as per. There are additional qualities: increase in the computing ability benefits the system by being able to process more intricate data and response at a faster speed. With technological enhancement, AVs are much more competent to encounter more conducting circumstances and environment outputs.

- Safety and Efficiency:

AVs shall have massive enhancement in road safety, and traffic flow congestion should be alleviated by them. For this reason, consumption of AVs removes the occurrences of human-made mistakes that account for accidents thereby leading to the improvement of collision rates and; overall road safety. With them, cars will be able to communicate with each other and other structures hence avoiding situations such as traffic jam. According to this, AVs has the potential of enhancing the manner in which vehicles can be driven with an aim of enhancing the fuel conservation and reduction of discharge of pollutants to the environment. Due to this, AVs are much more appealing than traditional vehicles since safety and efficiency are always of high importance to everyone.

- Regulatory Support:

The market for AVs can only progress with the support of legislative angles. National and/or regional governments across the world are putting in place mechanisms and recommendations for AVs design, evaluation, and use. This includes issues to do with formulation of safety regulations, formulation of liability rules, rules to do with data security and data privacy. Other measures such as funding and tax credits for the promotion of innovative solutions may also have an impact on the development of the AV segment. With the change in regulatory environments, AV technology brings along reduction in uncertainties in the transport systems and enhance integration of the technology.

We explore the factors propelling the autonomous vehicle market growth, including technological advancements, consumer behaviors, and regulatory changes.

Leading Companies Operating in the Global Autonomous Vehicle Industry:

- AB Volvo

- AUDI Aktiengesellschaft (Volkswagen Group)

- Bayerische Motoren Werke AG

- Daimler AG

- Ford Motor Company

- General Motors

- Tesla Inc.

- Toyota Motor Corporation

- Uber Technologies Inc.

- Waymo LLC (Alphabet Inc.)

Autonomous Vehicle Market Report Segmentation:

By Component:

- Hardware

- Software and Services

Software and services represent the largest segment due to the rising focus on enhancing the capabilities, safety, and functionality of autonomous vehicles.

By Level of Automation:

- Level 3

- Level 4

- Level 5

Level 3 holds the biggest market share as it provides a balance between autonomous driving convenience and the need for human oversight.

By Application:

- Transportation and Logistics

- Military and Defense

Transportation and logistics account for the largest market share on account of the increasing need for more efficient last-mile delivery solutions.

Regional Insights:

- North America: (United States, Canada)

- Asia Pacific: (China, Japan, India, South Korea, Australia, Indonesia, Others)

- Europe: (Germany, France, United Kingdom, Italy, Spain, Russia, Others)

- Latin America: (Brazil, Mexico, Others)

- Middle East and Africa

North America enjoys the leading position in the autonomous vehicle market, which can be attributed to the rising adoption of personal cars to travel conveniently.

Global Autonomous Vehicle Market Trends:

The time has come to use AVs because of the benefits they are believed to bring, such as added ease, safety, and comfort. According to Carberry et al., AVs provide an improved means of transport than conventional cars for immobile people like the elder or the disabled. Furthermore, traffic accidents and better driving experience also make users interested in using the promise.

Besides this, major investments from tech companies automobile giants and venture capitalists are fueling the AV tech research and its commercialization. Moreover, AVs can be connected with electric vehicle technology, and the uses of technology are helpful for lowering emissions and contributing to more sustainable goals.

Note: If you need specific information that is not currently within the scope of the report, we will provide it to you as a part of the customization.

About Us:

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provide a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: [email protected]

Tel No:(D) +91 120 433 0800

United States: +1-631-791-1145 | United Kingdom: +44-753-713-2163

IMARC Group's report titled "Autonomous Vehicle Market Report by Component (Hardware, Software and Services), Level of Automation (Level 3, Level 4, Level 5), Application (Transportation and Logistics, Military and Defense), and Region 2024-2032". The global autonomous vehicle market size reached USD 109.0 Billion in 2024. Looking forward, IMARC Group expects the market to reach USD 1,730.4 Billion by 2033, exhibiting a growth rate(CAGR) of 31.85% during 2025-2033.

For an in-depth analysis, you can refer sample copy of the report: https://www.imarcgroup.com/autonomous-vehicle-market/requestsample

Factors Affecting the Growth of the Autonomous Vehicle Industry:

- Technological Advancements:

Progresses are on the innovations aspects in the development of the autonomous vehicle (AV). New improvements in AI and ML technologies can let AVs understand the extensive information flowing from the environment and respond instantly to optimize safety and efficacy. The administration coming from these techniques of sensors, including LIDAR, radar, and cameras, offers the right data for these types of algorithms to operate effectively as per. There are additional qualities: increase in the computing ability benefits the system by being able to process more intricate data and response at a faster speed. With technological enhancement, AVs are much more competent to encounter more conducting circumstances and environment outputs.

- Safety and Efficiency:

AVs shall have massive enhancement in road safety, and traffic flow congestion should be alleviated by them. For this reason, consumption of AVs removes the occurrences of human-made mistakes that account for accidents thereby leading to the improvement of collision rates and; overall road safety. With them, cars will be able to communicate with each other and other structures hence avoiding situations such as traffic jam. According to this, AVs has the potential of enhancing the manner in which vehicles can be driven with an aim of enhancing the fuel conservation and reduction of discharge of pollutants to the environment. Due to this, AVs are much more appealing than traditional vehicles since safety and efficiency are always of high importance to everyone.

- Regulatory Support:

The market for AVs can only progress with the support of legislative angles. National and/or regional governments across the world are putting in place mechanisms and recommendations for AVs design, evaluation, and use. This includes issues to do with formulation of safety regulations, formulation of liability rules, rules to do with data security and data privacy. Other measures such as funding and tax credits for the promotion of innovative solutions may also have an impact on the development of the AV segment. With the change in regulatory environments, AV technology brings along reduction in uncertainties in the transport systems and enhance integration of the technology.

We explore the factors propelling the autonomous vehicle market growth, including technological advancements, consumer behaviors, and regulatory changes.

Leading Companies Operating in the Global Autonomous Vehicle Industry:

- AB Volvo

- AUDI Aktiengesellschaft (Volkswagen Group)

- Bayerische Motoren Werke AG

- Daimler AG

- Ford Motor Company

- General Motors

- Tesla Inc.

- Toyota Motor Corporation

- Uber Technologies Inc.

- Waymo LLC (Alphabet Inc.)

Explore the full report with table of contents: https://www.imarcgroup.com/autonomous-vehicle-market

Autonomous Vehicle Market Report Segmentation:

By Component:

- Hardware

- Software and Services

Software and services represent the largest segment due to the rising focus on enhancing the capabilities, safety, and functionality of autonomous vehicles.

By Level of Automation:

- Level 3

- Level 4

- Level 5

Level 3 holds the biggest market share as it provides a balance between autonomous driving convenience and the need for human oversight.

By Application:

- Transportation and Logistics

- Military and Defense

Transportation and logistics account for the largest market share on account of the increasing need for more efficient last-mile delivery solutions.

Regional Insights:

- North America: (United States, Canada)

- Asia Pacific: (China, Japan, India, South Korea, Australia, Indonesia, Others)

- Europe: (Germany, France, United Kingdom, Italy, Spain, Russia, Others)

- Latin America: (Brazil, Mexico, Others)

- Middle East and Africa

North America enjoys the leading position in the autonomous vehicle market, which can be attributed to the rising adoption of personal cars to travel conveniently.

Global Autonomous Vehicle Market Trends:

The time has come to use AVs because of the benefits they are believed to bring, such as added ease, safety, and comfort. According to Carberry et al., AVs provide an improved means of transport than conventional cars for immobile people like the elder or the disabled. Furthermore, traffic accidents and better driving experience also make users interested in using the promise.

Besides this, major investments from tech companies automobile giants and venture capitalists are fueling the AV tech research and its commercialization. Moreover, AVs can be connected with electric vehicle technology, and the uses of technology are helpful for lowering emissions and contributing to more sustainable goals.

Note: If you need specific information that is not currently within the scope of the report, we will provide it to you as a part of the customization.

About Us:

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provide a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: [email protected]

Tel No:(D) +91 120 433 0800

United States: +1-631-791-1145 | United Kingdom: +44-753-713-2163

Portable Generator Industry

Summary:

- The global portable generator market size reached USD 5.5 Billion in 2024.

- The market is expected to reach USD 8.9 Billion by 2033 exhibiting a growth rate (CAGR) of 5.41% during 2025-2033.

- Asia Pacific leads the market, accounting for the largest portable generator market share.

- Portable diesel generators hold the majority of the market share in the fuel type segment.

- Residential dominates the portable generator industry.

- Less than 3 kW represents the biggest application segment.

- The increasing demand for reliable backup power solutions is a primary driver of the portable generator market.

- Technological advancements and the rising use in healthcare and emergency services are reshaping the portable generator market.

Industry Trends and Drivers:

- Growing demand for reliable backup power solutions:

There is a rise in demand for dependable backup power sources as households and businesses seek solutions to counter frequent power outages, often resulting from extreme weather events and a deteriorating power grid infrastructure. Portable generators serve as convenient and cost-effective options for residential settings, allowing families to maintain essential electrical operations during unexpected blackouts. The shift to remote work further supports this demand, as continuous power is vital for internet connectivity, home office setups, and maintaining productivity. Additionally, these generators are less expensive and more accessible than stationary systems, widening their appeal across different demographics. The heightened awareness about emergency preparedness, coupled with a rising focus on resilient energy solutions, is encouraging individuals to adopt portable generators as essential household assets.

- Rising use in healthcare and emergency services:

The growing reliance on portable generators in the healthcare sector to ensure continuous power for critical equipment during emergencies and power outages is offering a favorable market outlook. In hospitals, clinics, and emergency response facilities, maintaining a steady power supply is essential for patient care, supporting lifesaving devices like ventilators, defibrillators, and surgical lights. Portable generators are also invaluable for emergency medical services (EMS) in remote or disaster-hit areas where stable infrastructure may be compromised or absent. Additionally, mobile healthcare units and temporary medical camps often use portable generators to establish dependable power sources. Healthcare and emergency service providers are expanding their reach into rural and underserved regions, which is driving the demand for portable generators.

- Technological advancements:

Advancements in generator technology are leading to the development of newer models offering higher fuel efficiency, lower emissions, and enhanced user control through smart features. Innovations like inverter generators are making it possible to provide cleaner, more stable power suitable for sensitive electronics, expanding the use cases of portable generators across various individual and commercial applications. Additionally, modern models often include features, including Bluetooth connectivity, remote monitoring, and mobile app integration, allowing users to control and monitor their generators from a distance. These advancements make portable generators more user-friendly, convenient, and reliable. The increasing user expectations and smart-home integration are leading to the adoption of portable generators with enhanced functionalities.

Request for a sample copy of this report: https://www.imarcgroup.com/portable-generator-market/requestsample

Portable Generator Market Report Segmentation:

Breakup By Fuel Type:

- Portable Diesel Generators

- Portable Gas Generators

- Others

Portable diesel generators exhibit a clear dominance in the market owing to their superior fuel efficiency, longer operational lifespans, and robust performance in various environments.

Breakup By Application:

- Residential

- Commercial

- Industrial

- Infrastructure

Residential holds the biggest market share, as homeowners rely on portable generators for backup power during outages and for enhancing the functionality of outdoor activities.

Breakup By Power Output:

- Less than 3 kW

- 3-10kW

- More than 10kW

Less than 3 kW represents the largest segment due to its affordability, portability, and adequacy for common residential and recreational power needs.

Breakup By Region:

- North America (United States, Canada)

- Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, Others)

- Europe (Germany, France, United Kingdom, Italy, Spain, Russia, Others)

- Latin America (Brazil, Mexico, Others)

- Middle East and Africa

Asia Pacific dominates the market, driven by the rising demand for reliable power solutions across the region.

Top Portable Generator Market Leaders:

The portable generator market research report outlines a detailed analysis of the competitive landscape, offering in-depth profiles of major companies. Some of the key players in the market are:

- Briggs & Stratton Corporation

- Cummins Inc.

- Honda Motor Co., Ltd.

- Eaton Corporation PLC

- Generac Power Systems Inc.

If you require any specific information that is not covered currently within the scope of the report, we will provide the same as a part of the customization.

About Us:

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provide a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: [email protected]

Tel No:(D) +91 120 433 0800

United States: +1-631-791-1145 | United Kingdom: +44-753-713-2163

Summary:

- The global medical coatings market size reached USD 2.1 Billion in 2023.

- The market is expected to reach USD 8.5 Billion by 2032, exhibiting a growth rate (CAGR) of 16.8% during 2024-2032.

- North America leads the market, accounting for the largest medical coatings market share.

- Hydrophilic coating holds the majority of the market share in the type segment.

- Polymers dominate the medical coatings industry.

- Medical device represents the biggest application segment.

- The rising demand for minimally invasive (MI) procedures is a primary driver of the medical coatings market.

- Technological advancements and the growing Increasing need for infection prevention are reshaping the medical coatings market.

Request for a sample copy of this report: https://www.imarcgroup.com/medical-coatings-market

Industry Trends and Drivers:

- Rising demand for minimally invasive (MI) procedures:

The increasing adoption of less invasive procedures, which prioritize patient comfort and reduce recovery times, is bolstering the market growth. These procedures require medical devices with specialized coatings that minimize friction and ensure smoother, more controlled navigation within the body. Medical coatings on devices, such as catheters, guidewires, and endoscopes, reduce trauma to surrounding tissue, lower the risk of infection, and enhance device maneuverability. Minimally invasive (MI) techniques are gaining traction across various medical fields like cardiology, neurology, orthopedics, and oncology, which is driving the demand for friction-reducing, non-reactive coatings. Technological advancements in less invasive surgery are encouraging manufacturers to develop more sophisticated coatings that can withstand prolonged use while maintaining safety.

- Increasing need for infection prevention:

The growing focus on infection prevention in healthcare is catalyzing the demand for medical coatings with antimicrobial properties. These coatings play a crucial role in combating healthcare-associated infections (HAIs), which pose a severe risk in clinical settings and account for considerable costs to healthcare systems. Antimicrobial coatings on medical devices like catheters, surgical instruments, and implantable devices effectively inhibit the growth of harmful bacteria and other pathogens. This is particularly important in sterile environments where even minimal contamination can lead to serious complications. The push from regulatory authorities for hospitals and clinics to adopt rigorous infection prevention measures is encouraging the adoption of these coatings. Manufacturers are developing advanced, long-lasting antimicrobial solutions that offer sustained protection on device surfaces.

- Technological advancements in coating materials:

Continuous advancements in coating technology are leading to the development of highly specialized and biocompatible materials. New materials, including fluoropolymers, silicone-based coatings, and hydrophilic formulations, improve device performance by enhancing lubricity, chemical resistance, and biocompatibility. Innovations in nanotechnology are further enabling the creation of ultra-thin, high-precision coatings that deliver superior functionality while minimizing patient risk. Hydrophilic coatings create a water-attracting surface that improves device maneuverability within the body, while fluoropolymer coatings provide exceptional chemical resistance, making them ideal for devices exposed to bodily fluids. These advanced coatings support the increasing trend of implantable and wearable medical devices, as they help ensure safe, long-term interaction with body tissues.

We explore the factors propelling the pharmacovigilance market growth, including technological advancements, consumer behaviors, and regulatory changes.

Medical Coatings Market Report Segmentation:

By Type:

- Hydrophilic Coating

- Anti-Microbial Coating

- Anti-Thrombogenic Coating

- Others

Hydrophilic coating exhibits a clear dominance in the market due to its superior biocompatibility and ability to enhance device functionality by reducing friction and improving lubrication.

By Material Type:

- Polymers

- Metals

- Others

Polymers represent the largest segment attributed to their versatility, cost-effectiveness, and ease of application on various medical devices.

By Application:

- Medical Device

- Medical Implants

- Medical Equipment and Tools

- Others

Medical device holds the biggest market share owing to the extensive use of coatings to improve device performance, safety, and longevity in clinical settings.

Regional Insights:

- North America (United States, Canada)

- Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, Others)

- Europe (Germany, France, United Kingdom, Italy, Spain, Russia, Others)

- Latin America (Brazil, Mexico, Others)

- Middle East and Africa

North America dominates the market, driven by advanced healthcare infrastructure, high investment in medical technology, and strong presence of leading medical device manufacturers.

Top Medical Coatings Market Leaders:

The medical coatings market research report outlines a detailed analysis of the competitive landscape, offering in-depth profiles of major companies. Some of the key players in the market are:

- Applied Medical Coatings LLC

- AST Products Inc.

- Biocoat Incorporated

- Harland Medical Systems Inc.

- Hydromer Inc.

- Koninklijke DSM N.V.

- Medicoat AG

- Merit Medical Systems Inc.

- Precision Coating Company Inc. (Katahdin Industries Inc.)

- Specialty Coating Systems Inc. (Kisco Ltd.), SurModics Inc.

If you require any specific information that is not covered currently within the scope of the report, we will provide the same as a part of the customization.

About Us:

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provide a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: [email protected]

Tel No:(D) +91 120 433 0800

United States: +1-631-791-1145 | United Kingdom: +44-753-713-2163

Pharmacovigilance Industry

Summary:

- The global pharmacovigilance market size reached USD 7.9 Billion in 2023.

- The market is expected to reach USD 15.9 Billion by 2032, exhibiting a growth rate (CAGR) of 7.8% during 2024-2032.

- North America leads the market, accounting for the largest pharmacovigilance market share.

- Contract outsourcing accounts for the majority of the market share in the service provider segment.

- Phase IV holds the largest share in the pharmacovigilance industry.

- Spontaneous reporting remains a dominant segment in the market.

- Signal detection (adverse event logging, adverse event analysis, and adverse event review and reporting) represents the leading process flow segment.

- Oncology holds the biggest market share.

- Pharmaceutical companies represent the leading segment.

- The rise in regulatory requirements and stringent safety standards is a primary driver of the pharmacovigilance market.

- The advent of advanced technologies, particularly artificial intelligence (AI) and machine learning (ML), is reshaping the pharmacovigilance market.

Industry Trends and Drivers:

- Increasing Regulatory Requirements and Stringent Safety Standards:

Governments and regulatory bodies worldwide are continually enhancing pharmacovigilance regulations to ensure the safety and efficacy of pharmaceutical products. Agencies and other national regulatory authorities have implemented more rigorous guidelines for post-marketing surveillance. These regulations mandate comprehensive reporting of adverse drug reactions (ADRs), periodic safety updates, and risk management plans. The introduction of regulations necessitates robust pharmacovigilance systems for compliance. Pharmaceutical companies must invest in sophisticated pharmacovigilance infrastructure to meet these standards, thereby impelling the market growth. Additionally, the globalization of drug markets requires harmonization of safety standards across regions, further increasing the demand for advanced pharmacovigilance solutions and services to navigate diverse regulatory landscapes effectively.

- Technological Advancements and Integration of AI in Pharmacovigilance:

The advent of advanced technologies, particularly artificial intelligence (AI) and machine learning (ML), is revolutionizing pharmacovigilance practices. These technologies enable the efficient processing and analysis of vast amounts of data from diverse sources, including electronic health records (EHRs), social media, and real-world evidence (RWE). AI-powered tools facilitate the automated detection of adverse drug reactions, signal identification, and trend analysis, significantly enhancing the accuracy and speed of pharmacovigilance activities. Additionally, natural language processing (NLP) aids in extracting relevant information from unstructured data, improving the comprehensiveness of safety monitoring. The integration of blockchain technology is also emerging to ensure data integrity and transparency in pharmacovigilance processes. These technological innovations not only streamline pharmacovigilance workflows but also reduce costs and minimize human error, making them attractive investments for pharmaceutical companies.

- Expansion of the Global Pharmaceutical Market and Increased Drug Development:

The global pharmaceutical market is experiencing significant expansion, driven by increasing investments in drug research and development (R&D) and the introduction of innovative therapies. As pharmaceutical companies develop a broader range of medications, including biologics, biosimilars, and personalized medicines, the complexity of monitoring drug safety is growing. The rise in chronic diseases and the aging population globally contribute to higher demand for diverse therapeutic options, necessitating comprehensive pharmacovigilance to manage the associated safety profiles. Additionally, the rise in clinical trials across different regions to support the globalization of drug development amplifies the need for robust pharmacovigilance systems to oversee multi-regional safety data. The expansion into emerging markets, where regulatory frameworks are evolving, also requires tailored pharmacovigilance strategies to ensure effective monitoring. This growth in the pharmaceutical sector, coupled with the increasing complexity of drug portfolios, drives the demand for specialized pharmacovigilance services and solutions.

Request for a sample copy of this report: https://www.imarcgroup.com/pharmacovigilance-market/requestsample

Pharmacovigilance Market Report Segmentation:

Breakup By Service Provider:

- In-house

- Contract Outsourcing

Contract outsourcing represents the largest segment as pharmaceutical companies increasingly seek specialized expertise and cost-effective solutions to manage complex safety monitoring requirements without the overhead of maintaining in-house teams.

Breakup By Product Life Cycle:

- Pre-clinical

- Phase I

- Phase II

- Phase III

- Phase IV

Phase IV dominates the market because post-marketing surveillance is crucial for ongoing safety assessment, regulatory compliance, and the identification of rare adverse effects.

Breakup By Type:

- Spontaneous Reporting

- Intensified ADR Reporting

- Targeted Spontaneous Reporting

- Cohort Event Monitoring

- EHR Mining

Spontaneous reporting exhibits are clear dominance in the market due to its widespread adoption as a fundamental method for capturing real-world adverse event data directly from healthcare professionals and patients.

Breakup By Process Flow:

- Case Data Management

- Case Logging

- Case Data Analysis

- Medical Reviewing and Reporting

- Signal Detection

- Adverse Event Logging

- Adverse Event Analysis

- Adverse Event Review and Reporting

- Risk Management System

- Risk Evaluation System

- Risk Mitigation System

Signal detection (adverse event logging, adverse event analysis, and adverse event review and reporting) accounts for the majority of the market share. It is essential for identifying potential safety issues through the systematic collection, analysis, and evaluation of adverse event data,

Breakup By Therapeutic Area:

- Oncology

- Neurology

- Cardiology

- Respiratory Systems

- Others

Oncology holds the biggest market share driven by the high incidence of adverse effects associated with cancer treatments and the critical need for rigorous safety monitoring to ensure patient safety and treatment efficacy in this complex and high-stakes field.

Breakup By End Use:

- Pharmaceuticals Companies

- Biotechnology Companies

- Medical Device Companies

- Others

Pharmaceutical companies represent the leading segment since they are primarily responsible for the development, approval, and post-marketing surveillance of drugs.

Breakup By Region:

- North America (United States, Canada)

- Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, Others)

- Europe (Germany, France, United Kingdom, Italy, Spain, Russia, Others)

- Latin America (Brazil, Mexico, Others)

- Middle East and Africa

North America enjoys the leading position attributed to its stringent regulatory framework, extensive healthcare infrastructure, and high pharmaceutical activity.

Top Pharmacovigilance Market Leaders:

The pharmacovigilance market research report outlines a detailed analysis of the competitive landscape, offering in-depth profiles of major companies. Some of the key players in the market are:

- Accenture plc

- ArisGlobal LLC

- BioClinica Inc. (Cinven Partners LLP)

- Capgemini

- Cognizant

- International Business Machines Corporation

- ICON plc.

- IQVIA Inc.

- ITClinical

- Parexel International Corporation

- Wipro Limited

If you require any specific information that is not covered currently within the scope of the report, we will provide the same as a part of the customization.

About Us:

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provide a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: [email protected]

Tel No:(D) +91 120 433 0800

United States: +1-631-791-1145 | United Kingdom: +44-753-713-2163

Pharmacovigilance Industry

Summary:

- The global pharmacovigilance market size reached USD 7.9 Billion in 2023.

- The market is expected to reach USD 15.9 Billion by 2032, exhibiting a growth rate (CAGR) of 7.8% during 2024-2032.

- North America leads the market, accounting for the largest pharmacovigilance market share.

- Contract outsourcing accounts for the majority of the market share in the service provider segment.

- Phase IV holds the largest share in the pharmacovigilance industry.

- Spontaneous reporting remains a dominant segment in the market.

- Signal detection (adverse event logging, adverse event analysis, and adverse event review and reporting) represents the leading process flow segment.

- Oncology holds the biggest market share.

- Pharmaceutical companies represent the leading segment.

- The rise in regulatory requirements and stringent safety standards is a primary driver of the pharmacovigilance market.

- The advent of advanced technologies, particularly artificial intelligence (AI) and machine learning (ML), is reshaping the pharmacovigilance market.

Industry Trends and Drivers:

- Increasing Regulatory Requirements and Stringent Safety Standards:

Governments and regulatory bodies worldwide are continually enhancing pharmacovigilance regulations to ensure the safety and efficacy of pharmaceutical products. Agencies and other national regulatory authorities have implemented more rigorous guidelines for post-marketing surveillance. These regulations mandate comprehensive reporting of adverse drug reactions (ADRs), periodic safety updates, and risk management plans. The introduction of regulations necessitates robust pharmacovigilance systems for compliance. Pharmaceutical companies must invest in sophisticated pharmacovigilance infrastructure to meet these standards, thereby impelling the market growth. Additionally, the globalization of drug markets requires harmonization of safety standards across regions, further increasing the demand for advanced pharmacovigilance solutions and services to navigate diverse regulatory landscapes effectively.

- Technological Advancements and Integration of AI in Pharmacovigilance:

The advent of advanced technologies, particularly artificial intelligence (AI) and machine learning (ML), is revolutionizing pharmacovigilance practices. These technologies enable the efficient processing and analysis of vast amounts of data from diverse sources, including electronic health records (EHRs), social media, and real-world evidence (RWE). AI-powered tools facilitate the automated detection of adverse drug reactions, signal identification, and trend analysis, significantly enhancing the accuracy and speed of pharmacovigilance activities. Additionally, natural language processing (NLP) aids in extracting relevant information from unstructured data, improving the comprehensiveness of safety monitoring. The integration of blockchain technology is also emerging to ensure data integrity and transparency in pharmacovigilance processes. These technological innovations not only streamline pharmacovigilance workflows but also reduce costs and minimize human error, making them attractive investments for pharmaceutical companies.

- Expansion of the Global Pharmaceutical Market and Increased Drug Development:

The global pharmaceutical market is experiencing significant expansion, driven by increasing investments in drug research and development (R&D) and the introduction of innovative therapies. As pharmaceutical companies develop a broader range of medications, including biologics, biosimilars, and personalized medicines, the complexity of monitoring drug safety is growing. The rise in chronic diseases and the aging population globally contribute to higher demand for diverse therapeutic options, necessitating comprehensive pharmacovigilance to manage the associated safety profiles. Additionally, the rise in clinical trials across different regions to support the globalization of drug development amplifies the need for robust pharmacovigilance systems to oversee multi-regional safety data. The expansion into emerging markets, where regulatory frameworks are evolving, also requires tailored pharmacovigilance strategies to ensure effective monitoring. This growth in the pharmaceutical sector, coupled with the increasing complexity of drug portfolios, drives the demand for specialized pharmacovigilance services and solutions.

Request for a sample copy of this report: https://www.imarcgroup.com/pharmacovigilance-market/requestsample

Pharmacovigilance Market Report Segmentation:

Breakup By Service Provider:

- In-house

- Contract Outsourcing

Contract outsourcing represents the largest segment as pharmaceutical companies increasingly seek specialized expertise and cost-effective solutions to manage complex safety monitoring requirements without the overhead of maintaining in-house teams.

Breakup By Product Life Cycle:

- Pre-clinical

- Phase I

- Phase II

- Phase III

- Phase IV

Phase IV dominates the market because post-marketing surveillance is crucial for ongoing safety assessment, regulatory compliance, and the identification of rare adverse effects.

Breakup By Type:

- Spontaneous Reporting

- Intensified ADR Reporting

- Targeted Spontaneous Reporting

- Cohort Event Monitoring

- EHR Mining

Spontaneous reporting exhibits are clear dominance in the market due to its widespread adoption as a fundamental method for capturing real-world adverse event data directly from healthcare professionals and patients.

Breakup By Process Flow:

- Case Data Management

- Case Logging

- Case Data Analysis

- Medical Reviewing and Reporting

- Signal Detection

- Adverse Event Logging

- Adverse Event Analysis

- Adverse Event Review and Reporting

- Risk Management System

- Risk Evaluation System

- Risk Mitigation System

Signal detection (adverse event logging, adverse event analysis, and adverse event review and reporting) accounts for the majority of the market share. It is essential for identifying potential safety issues through the systematic collection, analysis, and evaluation of adverse event data,

Breakup By Therapeutic Area:

- Oncology

- Neurology

- Cardiology

- Respiratory Systems

- Others

Oncology holds the biggest market share driven by the high incidence of adverse effects associated with cancer treatments and the critical need for rigorous safety monitoring to ensure patient safety and treatment efficacy in this complex and high-stakes field.

Breakup By End Use:

- Pharmaceuticals Companies

- Biotechnology Companies

- Medical Device Companies

- Others

Pharmaceutical companies represent the leading segment since they are primarily responsible for the development, approval, and post-marketing surveillance of drugs.

Breakup By Region:

- North America (United States, Canada)

- Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, Others)

- Europe (Germany, France, United Kingdom, Italy, Spain, Russia, Others)

- Latin America (Brazil, Mexico, Others)

- Middle East and Africa

North America enjoys the leading position attributed to its stringent regulatory framework, extensive healthcare infrastructure, and high pharmaceutical activity.

Top Pharmacovigilance Market Leaders:

The pharmacovigilance market research report outlines a detailed analysis of the competitive landscape, offering in-depth profiles of major companies. Some of the key players in the market are:

- Accenture plc

- ArisGlobal LLC

- BioClinica Inc. (Cinven Partners LLP)

- Capgemini

- Cognizant

- International Business Machines Corporation

- ICON plc.

- IQVIA Inc.

- ITClinical

- Parexel International Corporation

- Wipro Limited

If you require any specific information that is not covered currently within the scope of the report, we will provide the same as a part of the customization.

About Us:

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provide a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: [email protected]

Tel No:(D) +91 120 433 0800

United States: +1-631-791-1145 | United Kingdom: +44-753-713-2163

Pharmacovigilance Industry

Summary:

- The global pharmacovigilance market size reached USD 7.9 Billion in 2023.

- The market is expected to reach USD 15.9 Billion by 2032, exhibiting a growth rate (CAGR) of 7.8% during 2024-2032.

- North America leads the market, accounting for the largest pharmacovigilance market share.

- Contract outsourcing accounts for the majority of the market share in the service provider segment.

- Phase IV holds the largest share in the pharmacovigilance industry.

- Spontaneous reporting remains a dominant segment in the market.

- Signal detection (adverse event logging, adverse event analysis, and adverse event review and reporting) represents the leading process flow segment.

- Oncology holds the biggest market share.

- Pharmaceutical companies represent the leading segment.

- The rise in regulatory requirements and stringent safety standards is a primary driver of the pharmacovigilance market.

- The advent of advanced technologies, particularly artificial intelligence (AI) and machine learning (ML), is reshaping the pharmacovigilance market.

Industry Trends and Drivers:

- Increasing Regulatory Requirements and Stringent Safety Standards:

Governments and regulatory bodies worldwide are continually enhancing pharmacovigilance regulations to ensure the safety and efficacy of pharmaceutical products. Agencies and other national regulatory authorities have implemented more rigorous guidelines for post-marketing surveillance. These regulations mandate comprehensive reporting of adverse drug reactions (ADRs), periodic safety updates, and risk management plans. The introduction of regulations necessitates robust pharmacovigilance systems for compliance. Pharmaceutical companies must invest in sophisticated pharmacovigilance infrastructure to meet these standards, thereby impelling the market growth. Additionally, the globalization of drug markets requires harmonization of safety standards across regions, further increasing the demand for advanced pharmacovigilance solutions and services to navigate diverse regulatory landscapes effectively.

- Technological Advancements and Integration of AI in Pharmacovigilance:

The advent of advanced technologies, particularly artificial intelligence (AI) and machine learning (ML), is revolutionizing pharmacovigilance practices. These technologies enable the efficient processing and analysis of vast amounts of data from diverse sources, including electronic health records (EHRs), social media, and real-world evidence (RWE). AI-powered tools facilitate the automated detection of adverse drug reactions, signal identification, and trend analysis, significantly enhancing the accuracy and speed of pharmacovigilance activities. Additionally, natural language processing (NLP) aids in extracting relevant information from unstructured data, improving the comprehensiveness of safety monitoring. The integration of blockchain technology is also emerging to ensure data integrity and transparency in pharmacovigilance processes. These technological innovations not only streamline pharmacovigilance workflows but also reduce costs and minimize human error, making them attractive investments for pharmaceutical companies.

- Expansion of the Global Pharmaceutical Market and Increased Drug Development:

The global pharmaceutical market is experiencing significant expansion, driven by increasing investments in drug research and development (R&D) and the introduction of innovative therapies. As pharmaceutical companies develop a broader range of medications, including biologics, biosimilars, and personalized medicines, the complexity of monitoring drug safety is growing. The rise in chronic diseases and the aging population globally contribute to higher demand for diverse therapeutic options, necessitating comprehensive pharmacovigilance to manage the associated safety profiles. Additionally, the rise in clinical trials across different regions to support the globalization of drug development amplifies the need for robust pharmacovigilance systems to oversee multi-regional safety data. The expansion into emerging markets, where regulatory frameworks are evolving, also requires tailored pharmacovigilance strategies to ensure effective monitoring. This growth in the pharmaceutical sector, coupled with the increasing complexity of drug portfolios, drives the demand for specialized pharmacovigilance services and solutions.

Request for a sample copy of this report: https://www.imarcgroup.com/pharmacovigilance-market/requestsample

Pharmacovigilance Market Report Segmentation:

Breakup By Service Provider:

- In-house

- Contract Outsourcing

Contract outsourcing represents the largest segment as pharmaceutical companies increasingly seek specialized expertise and cost-effective solutions to manage complex safety monitoring requirements without the overhead of maintaining in-house teams.

Breakup By Product Life Cycle:

- Pre-clinical

- Phase I

- Phase II

- Phase III

- Phase IV

Phase IV dominates the market because post-marketing surveillance is crucial for ongoing safety assessment, regulatory compliance, and the identification of rare adverse effects.

Breakup By Type:

- Spontaneous Reporting

- Intensified ADR Reporting

- Targeted Spontaneous Reporting

- Cohort Event Monitoring

- EHR Mining

Spontaneous reporting exhibits are clear dominance in the market due to its widespread adoption as a fundamental method for capturing real-world adverse event data directly from healthcare professionals and patients.

Breakup By Process Flow:

- Case Data Management

- Case Logging

- Case Data Analysis

- Medical Reviewing and Reporting

- Signal Detection

- Adverse Event Logging

- Adverse Event Analysis

- Adverse Event Review and Reporting

- Risk Management System

- Risk Evaluation System

- Risk Mitigation System

Signal detection (adverse event logging, adverse event analysis, and adverse event review and reporting) accounts for the majority of the market share. It is essential for identifying potential safety issues through the systematic collection, analysis, and evaluation of adverse event data,

Breakup By Therapeutic Area:

- Oncology

- Neurology

- Cardiology

- Respiratory Systems

- Others

Oncology holds the biggest market share driven by the high incidence of adverse effects associated with cancer treatments and the critical need for rigorous safety monitoring to ensure patient safety and treatment efficacy in this complex and high-stakes field.

Breakup By End Use:

- Pharmaceuticals Companies

- Biotechnology Companies

- Medical Device Companies

- Others

Pharmaceutical companies represent the leading segment since they are primarily responsible for the development, approval, and post-marketing surveillance of drugs.

Breakup By Region:

- North America (United States, Canada)

- Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, Others)

- Europe (Germany, France, United Kingdom, Italy, Spain, Russia, Others)

- Latin America (Brazil, Mexico, Others)

- Middle East and Africa

North America enjoys the leading position attributed to its stringent regulatory framework, extensive healthcare infrastructure, and high pharmaceutical activity.

Top Pharmacovigilance Market Leaders:

The pharmacovigilance market research report outlines a detailed analysis of the competitive landscape, offering in-depth profiles of major companies. Some of the key players in the market are:

- Accenture plc

- ArisGlobal LLC

- BioClinica Inc. (Cinven Partners LLP)

- Capgemini

- Cognizant

- International Business Machines Corporation

- ICON plc.

- IQVIA Inc.

- ITClinical

- Parexel International Corporation

- Wipro Limited

If you require any specific information that is not covered currently within the scope of the report, we will provide the same as a part of the customization.

About Us:

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provide a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: [email protected]

Tel No:(D) +91 120 433 0800

United States: +1-631-791-1145 | United Kingdom: +44-753-713-2163

Boom Lifts Industry

Summary:

- The global boom lifts market size reached USD 11.8 Billion in 2023.

- The market is expected to reach USD 18.9 Billion by 2032, exhibiting a growth rate (CAGR) of 5.4% during 2024-2032.

- North America leads the market, accounting for the largest boom lifts market share.

- On the basis of the engine type, the market has been bifurcated into electric and engine-powered.

- Vehicle mounted booms account for the majority of the market share in the product type segment as they aid in providing flexibility and efficiency in urban areas with limited space.

- Rental holds the largest share in the boom lifts industry.

- The thriving construction sector is a primary driver of the boom lifts market.

- The rising focus on worker safety and technological advancements are reshaping the boom lifts market.

Request for a sample copy of this report: https://www.imarcgroup.com/boom-lifts-market/requestsample

Industry Trends and Drivers:

- Thriving Construction Industry:

The growing demand for boom lifts due to the thriving construction industry is offering a favorable market outlook. Increasing investments in commercial and residential spaces create a high demand for machinery that can provide safe and efficient access to elevated work areas. Boom lifts are essential for jobs like painting, window installation, facade work, and structural inspections. In addition, governing agencies of various countries are focusing on smart cities and large-scale infrastructure projects, which are supporting the market growth. Besides this, the rising need for equipment that offers high reach, stability, and versatility is contributing to the market growth. Boom lifts cater to these needs, enhancing productivity while ensuring worker safety at heights.

- Rising Focus on Worker Safety:

Worker safety regulations are becoming more stringent across industries, which is impelling the market growth. These machines offer a safer alternative to traditional scaffolding, ladders, and other lifting equipment, especially for tasks performed at heights. Boom lifts come with advanced safety features, such as stability control, emergency lowering systems, and harness attachment points, significantly reducing the risk of falls and accidents. Compliance with safety standards, particularly in construction, maintenance, and industrial sectors, is making the use of boom lifts a priority for companies looking to minimize workplace hazards. The Occupational Safety and Health Administration (OSHA) and other safety authorities worldwide advocate for the use of such equipment to reduce worksite injuries.

- Technological Advancements:

The integration of innovative technologies into boom lifts is driving market growth. Electric and hybrid boom lifts are gaining popularity due to their eco-friendly features, including reduced emissions and lower noise levels. This is particularly important for indoor or urban projects where emissions and noise restrictions are stringent. Additionally, advancements in telematics allow remote monitoring of equipment, improving efficiency and predictive maintenance. The development of lightweight and more energy-efficient models also reduces operational costs and expands the range of potential applications. These technological innovations cater to evolving user demands for eco-conscious, cost-effective, and safer equipment, making the new generation of boom lifts more attractive in the global market.

We explore the factors driving the growth of the market, including technological advancements, consumer behaviors, and regulatory changes, along with emerging boom lifts market trends.

Boom Lifts Market Report Segmentation:

Breakup By Engine Type:

- Electric

- Engine-powered

On the basis of the engine type, the market has been bifurcated into electric and engine-powered.

Breakup By Product Type:

- Trailer Mounted Booms

- Vehicle Mounted Booms

- Crawler/Spider Booms

Vehicle mounted booms accounted for the largest market share because they offer enhanced mobility and versatility, making them ideal for various applications in construction, maintenance, and landscaping.

Breakup By End Use:

- Rental

- Construction and Building

- Mining

- Transportation and Logistics

- Landscaping and Orchard Work

- Others

Rental represents the leading segment due to the flexibility it provides contractors and businesses, allowing them to access boom lifts without the financial burden of ownership, particularly for short-term projects.

Breakup By Region:

- North America (United States, Canada)

- Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, Others)

- Europe (Germany, France, United Kingdom, Italy, Spain, Russia, Others)

- Latin America (Brazil, Mexico, Others)

- Middle East and Africa

North America's dominance in the boom lifts market is attributed to its strong construction and infrastructure development activities, combined with a high adoption rate of advanced aerial work platforms across various industries.

Top Boom Lifts Market Leaders:

The boom lifts market research report outlines a detailed analysis of the competitive landscape, offering in-depth profiles of major companies. Some of the key players in the market are:

- Dexterlifts Oy

- Dinolift Oy

- Galmon (S) Pte Ltd

- Haulotte Group SA

- JLG Industries, Inc. (Oshkosh Corporation)

- Leguan Lifts Oy (Avant Tecno Group)

- Niftylift (UK) Limited

- Skyjack Inc (Linamar Corporation)

- Teupen Maschinenbau GmbH

- Xuzhou Construction Machinery Group Co., Ltd.

- Zoomlion Heavy Industry Science&Technology Co., Ltd.

If you require any specific information that is not covered currently within the scope of the report, we will provide the same as a part of the customization.

About Us:

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provide a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: [email protected]

Tel No:(D) +91 120 433 0800

United States: +1-631-791-1145 | United Kingdom: +44-753-713-2163

Global Commercial Seaweeds Market Statistics: USD 42.3 Billion Value by 2032

Commercial Seaweeds Industry

Summary:

- The global commercial seaweeds market size reached USD 21.4 Billion in 2023.

- The market is expected to reach USD 42.3 Billion by 2032, exhibiting a growth rate (CAGR) of 7.9% during 2024–2032.

- Asia Pacific leads the market, accounting for the largest commercial seaweeds market share.

- Red seaweeds account for the majority of the market share in the product segment due to their use in the cosmetic industry.

- Liquid holds the largest share in the commercial seaweeds industry.

- Human consumption remains a dominant segment in the market owing to the growing demand for seaweed-based supplements among the masses.

- The rising awareness about sustainability is a primary driver of the commercial seaweeds market.

- The growing demand for healthy food products is reshaping the commercial seaweeds market.

Request for a sample copy of this report: https://www.imarcgroup.com/commercial-seaweeds-market/requestsample

Industry Trends and Drivers:

- Rising awareness about sustainability:

Seaweeds are cultivated through sustainable and eco-friendly methods. They require minimal freshwater and do not rely on arable land, reducing the environmental footprint compared to traditional agriculture. Seaweeds can absorb carbon dioxide (CO2) from the atmosphere during their growth. This carbon sequestration potential is increasingly recognized as a valuable contribution to mitigating climate change. In addition, seaweed farming does not compete with land-based agriculture, which can help alleviate pressure on limited arable land resources, addressing global food security concerns.

- Growing demand for healthy food products:

Seaweeds are rich in vitamins, iodine, calcium, iron, and antioxidants. These nutritional benefits align with increasing preferences of people for healthier food options. Seaweeds are low in calories and fat, making them an attractive choice for individuals looking to manage their weight and maintain a balanced diet. They are naturally plant-based and vegan, making them a suitable choice for those following vegetarian or vegan diets. As these dietary preferences are becoming more popular, the demand for seaweed-based products is increasing.

- Innovations in seaweed-based products:

Ongoing innovations are leading to a wide range of seaweed-based products, including snacks, condiments, cosmetics, supplements, and biodegradable packaging. This diversification attracts a broader consumer base. Seaweed-based supplements and health products are gaining traction due to their potential health benefits. Innovations in these products cater to consumers seeking natural remedies and nutritional support. Besides this, chefs and food manufacturers are exploring creative ways to incorporate seaweeds into culinary dishes, introducing unique flavors and textures to the market.

We explore the factors propelling the commercial seaweeds market growth, including technological advancements, consumer behaviors, and regulatory changes.

Commercial Seaweeds Market Report Segmentation:

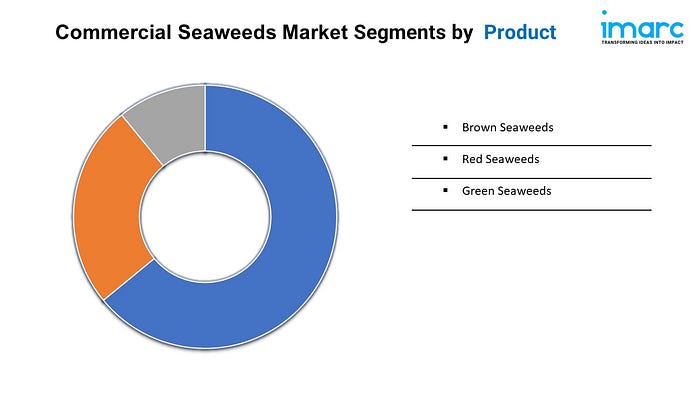

Breakup By Product:

- Brown Seaweeds

- Red Seaweeds

- Green Seaweeds

Red seaweeds represent the largest segment as they are widely used in the production of carrageenan, a versatile ingredient with various applications in the pharmaceutical industry.

Breakup By Form:

- Liquid

- Powdered

- Flakes

Liquid accounts for the majority of the market share due to the popularity of liquid seaweed extracts used as fertilizers in agriculture and plant growth enhancers.

Breakup By Application:

- Agriculture

- Animal Feed

- Human Consumption

- Others

Human consumption exhibits a clear dominance in the market owing to the increasing demand for seaweed-based food products and snacks.

Breakup By Region:

- North America (United States, Canada)

- Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, Others)

- Europe (Germany, France, United Kingdom, Italy, Spain, Russia, Others)

- Latin America (Brazil, Mexico, Others)

- Middle East and Africa

Asia Pacific enjoys the leading position in the commercial seaweeds market on account of its abundant seaweed resources and increasing practices of seaweed farming.

Top Commercial Seaweeds Market Leaders:

The commercial seaweeds market research report outlines a detailed analysis of the competitive landscape, offering in-depth profiles of major companies. Some of the key players in the market are:

- Acadian Seaplants Limited

- Algaia SA (Maabarot Products Ltd.)

- Biostadt India Limited

- BrandT Consolidated Inc.

- Cargill Incorporated

- COMPO Expert GmbH

- CP Kelco U.S. Inc (J.M. Huber Corporation)

- DuPont de Nemours Inc.

- Gelymar S.A.

- Indigrow Ltd.

- Lonza Group AG

- Seasol International Pty. Ltd.

- TBK Manufacturing Corporation

If you require any specific information that is not covered currently within the scope of the report, we will provide the same as a part of the customization.

About Us:

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provide a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: [email protected]

Tel No:(D) +91 120 433 0800

United States: +1–631–791–1145 | United Kingdom: +44–753–713–2163

Commercial Printing Industry

Summary:

- The global commercial printing market size reached USD 766.7 Billion in 2023.

- The market is expected to reach USD 841.9 Billion by 2032, exhibiting a growth rate (CAGR) of 1% during 2024–2032.

- Asia Pacific leads the market, accounting for the largest commercial printing market share.

- Lithographic printing accounts for the majority of the market share in the technology segment, as it provides high-quality and cost-effective solutions.

- Image holds the largest share in the commercial printing industry.

- Packaging remains a dominant segment in the market owing to the rising utilization of commercial printing in product packaging.

- The rising need for marketing and advertising is a primary driver of the commercial printing market.

- Technological advancements and customization trends are reshaping the commercial printing market.

Industry Trends and Drivers:

- Marketing and advertising needs:

Marketing campaigns often require a variety of printed materials, such as brochures, flyers, posters, and banners, to promote products or events. These materials are essential for creating awareness and attracting potential consumers. Businesses use printed materials to reinforce their brand identity as items like business cards, letterheads, and envelopes with consistent branding elements help create a professional and memorable image. Marketers send printed postcards, catalogs, and newsletters to targeted audiences, seeking to generate leads, drive sales, and foster customer loyalty.

- Customization trends:

Customization allows businesses to create personalized marketing materials. This includes personalized direct mail pieces, catalogs, and brochures that address recipients by name and feature content tailored as per their preferences and behavior. Variable data printing (VDP) technology enables the inclusion of unique text, images, and other elements in each printed piece within a single print run. This level of customization is invaluable for targeted marketing campaigns and enhancing engagement. Businesses can also segment their consumer base and create customized materials for different customer groups.

- Technological advancements:

Digital printing technology allows for quick and cost-effective production of high-quality printed materials without the need for traditional printing plates. This flexibility enables businesses to order smaller print runs and personalize content. Advancements in print head technology, color management, and inks are significantly improving the print quality of digital and offset printing. This enhanced quality appeals to businesses seeking polished and eye-catching marketing materials.

Request for a sample copy of this report: https://www.imarcgroup.com/commercial-printing-market/requestsample

Commercial Printing Market Report Segmentation:

Breakup By Technology:

- Lithographic Printing

- Digital Printing

- Flexographic Printing

- Screen Printing

- Gravure Printing

- Others

Lithographic printing represents the largest segment as it is a well-established and versatile printing method that caters to a wide range of industries and applications.

Breakup By Print Type:

- Image

- Painting

- Pattern

- Others

Image accounts for the majority of the market share due to the rising demand for images in various printed materials, including marketing collateral, packaging, and promotional materials.

Breakup By Application:

- Packaging

- Advertising

- Publishing

Packaging exhibits a clear dominance in the market owing to the reliance of the packaging industry on printed materials for labels and boxes.

Breakup By Region:

- North America (United States, Canada)

- Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, Others)

- Europe (Germany, France, United Kingdom, Italy, Spain, Russia, Others)

- Latin America (Brazil, Mexico, Others)

- Middle East and Africa

Asia Pacific enjoys the leading position in the commercial printing market on account of its robust manufacturing sector and rapid urbanization.

Top Commercial Printing Market Leaders:

The commercial printing market research report outlines a detailed analysis of the competitive landscape, offering in-depth profiles of major companies. Some of the key players in the market are:

- Quad/Graphics Inc.

- Dai Nippon Printing Co. Limited

- ACME Printing Inc

- RR Donnelley & Sons Company

- WestRock Company

- Quebecor World Inc.

- Toppan Co. Limited

- TC Transcontinental Inc.

- Cimpress plc

- Taylor Communications

- HH Global Ltd.

- Lagardere SCA

If you require any specific information that is not covered currently within the scope of the report, we will provide the same as a part of the customization.

About Us:

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provide a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: [email protected]

Tel No:(D) +91 120 433 0800

United States: +1–631–791–1145 | United Kingdom: +44–753–713–2163